Simply connect your exchange accounts and wallets to Crypto Tax Calculator and our software will calculate your capital gains, income and deductions. Get a crypto tax report ready to submit to HMRC or your accountant.

Quick summary of how to calculate your crypto tax in the UK

Step 1 – Record keeping: Maintain detailed records of all crypto transactions in GBP, including dates, transaction types, fees, and valuations, to ensure accurate tax reporting.

Step 2 – Identify taxable events: Determine which transactions, such as selling or swapping crypto, trigger a Capital Gains Tax (CGT) or Income Tax liability under UK law.

Step 3 – Calculate your average cost basis: Use HMRC's average cost basis method to calculate the cost of your cryptocurrency holdings for capital gains calculations.

Step 4 – Apply special HMRC rules: Account for the "Same Day" and "Bed and Breakfast" rules that adjust cost basis for trades made on the same day or within 30 days.

Step 5 – Deduct fees: Deduct transaction-related fees, such as exchange or gas fees, to reduce your taxable gains, provided they meet HMRC's criteria.

Step 6 – Calculate capital gains or losses: Subtract your adjusted cost basis and fees from the proceeds of each taxable event to determine your capital gains or losses.

Step 7 – Calculate income from crypto activities: Identify income-earning crypto activities like staking or mining, and calculate their taxable value in GBP at the time of receipt.

Step 8 – Calculate your tax liability: Combine your crypto-related capital gains, losses, and income with other taxable income to calculate your total tax owed for the year.

Why you can trust this guide: This guide was co-authored by Alexander Holm, a personal tax specialist at BKL, an accountancy and tax advisory firm based in London. Alexander has nearly a decade of experience helping clients with cryptoassets and crypto-related projects. His expertise enables us to provide you with the most up-to-date information about crypto tax in the UK.

Investment vs trading

In most cases of buying and selling cryptocurrency as a retail investor, you are participating in investing rather than trading. The two are treated differently for tax purposes.

Investing is subject to capital gains tax or income tax, depending on the nature of the transaction.

Trading in this case refers to self-employment which is subject to income tax and National Insurance Contributions.

The key difference between investing and Trading – along with the different tax treatments, is how losses generated in the crypto-activity can be used.

In their guidance, HMRC have explicitly stated that they would expect it to be exceedingly rare that any crypto-activity constituting buying & selling crypto would be classified as “trading”.

If you are uncertain, speak to a tax advisor as there are always exceptions, including but not limited to, developing tokens and large scale mining.

Do I still have to pay tax if my crypto was hacked, lost or stolen?

If your wallets or exchanges are hacked and the tokens stolen, this cannot be claimed as a loss.

HMRC's reasoning behind this is that you remain the legal owner of the tokens, despite not being able to access them, and therefore you cannot have made a loss as that would require a disposal or destruction of the asset. You can, however, pursue legal action against a counterparty responsible for the lost or stolen crypto.

CGT events occur when you dispose of your cryptocurrency.

"Disposal" includes selling, trading, or gifting crypto assets (except to a spouse or civil partner).

Each event triggers a CGT liability if the transaction results in a gain.

However, recording losses is equally important, as they can offset gains and reduce your overall tax burden.

How Investing vs Trading impacts tax

In most cases of buying and selling cryptocurrency as a retail investor, you are participating in investing rather than trading. The two are treated differently for tax purposes.

Investing is subject to capital gains tax or income tax, depending on the nature of the transaction.

Trading in this case refers to self-employment which is subject to income tax and National Insurance Contributions.

The key difference between investing and trading – along with the different tax treatments, is how losses generated in the crypto-activity can be used.

In their guidance, HMRC have explicitly stated that they would expect it to be exceedingly rare that any crypto-activity constituting buying & selling crypto would be classified as “trading”.

If you are uncertain, speak to a tax advisor as there are always exceptions, including but not limited to, developing tokens and large scale mining.

The easy way to classify taxable events in crypto

If you're an active trader or use DeFi a lot, then you're probably breaking into a cold sweat at the idea of accurately classifying all of your transactions.

The good news is that software like Crypto Tax Calculator can do that for you. Simply connect your exchange and wallet accounts and our software will do the rest.

After it's done analysing your crypto transactions, it will produce a tax report ready to submit to the HMRC or your tax agent. It can even handle the most complicated DeFi transactions like liquidity pools, cross-chain swaps, wrapping tokens and airdrops.

No need for stress, long nights spent hunched over spreadsheets or expensive accountant fees. Let Crypto Tax Calcualtor solve your crypto tax nightmare for you.

Stop over paying on your tax: Use Crypto Tax Calculator to automate your fee accounting and help ensure you’re getting the deductions you’re entitled to.

Crypto Tax Calculator automatically categorises your fees into deductible and non-deductible types, which are factored into your tax report. You can even override this and add any fees which you think should – or should not – be included in the deductible amount.

Don't miss out on deductions: Software like Crypto Tax Calculator will calculate your capital gains or losses for you and automatically offset any gains with eligible deductions like losses and gas fees.

Crypto Tax Calculator also has a Tax Loss Harvesting tool which can help you identify loss-making assets that can be sold to lower your total capital gains.

Get Your Tax Reports: Generate comprehensive tax reports ready for your accountant or tax authority.

If you're new to Crypto Tax Calculator, start with our Getting Started Guide for an overview of how the platform works.

Need more help? Visit our UK Report Guides or explore the Help Centre for step-by-step instructions.

2025-01-17

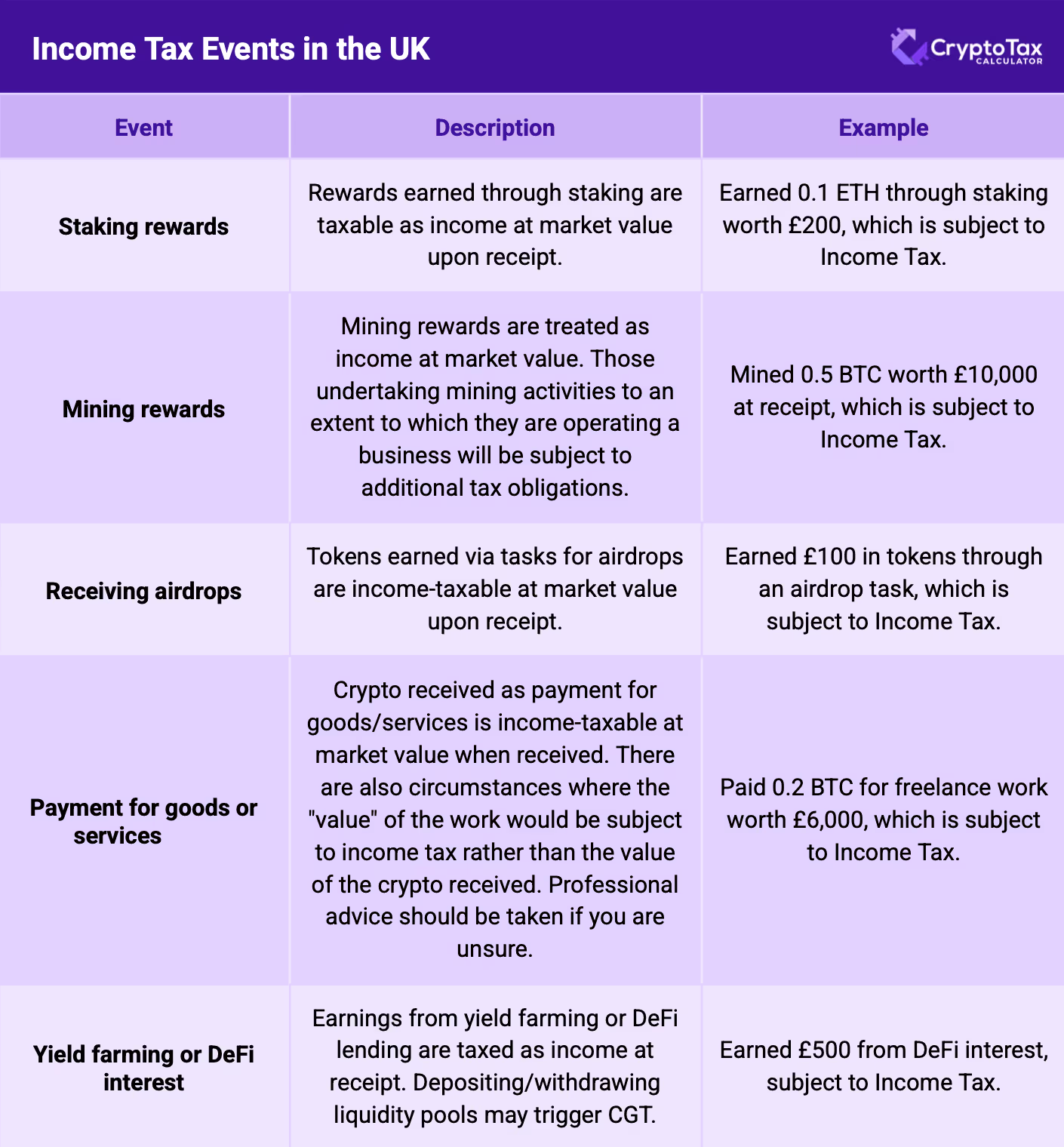

Yield farming or DeFi interest

Earnings from yield farming or lending crypto in DeFi platforms are taxed as income at the time they are received. However, depositing into and withdrawing from a liquidity pool may be treated as a disposal, which is a capital gains event.

Example: Earning £500 in interest from a DeFi platform is subject to Income Tax.

Payments for goods or services

Receiving cryptocurrency as payment for goods or services is treated as income at its market value when received. There are instances where the “value” of the work will be taxed instead of the value of the crypto received. Professional advice should be taken if you are unsure.

Example: If you're paid 0.2 BTC for freelance work worth £6,000, this amount is subject to Income Tax.

Receiving airdrops

If you actively participate to receive an airdrop (e.g., completing tasks), the tokens are treated as income at their market value upon receipt.

Example: Earning £100 in tokens from an airdrop after completing tasks is subject to Income Tax.

Mining rewards

Mining rewards are taxed as income. Those undertaking mining activities to an extent to which they are operating a business will be subject to additional tax obligations.

Example: Earning 0.5 BTC through mining worth £10,000 at the time of receipt is subject to Income Tax.

Staking rewards

Cryptocurrency earned through staking is considered income at the market value at the time of receipt.

Example: If you earn 0.1 ETH through staking worth £200, this amount is subject to Income Tax.

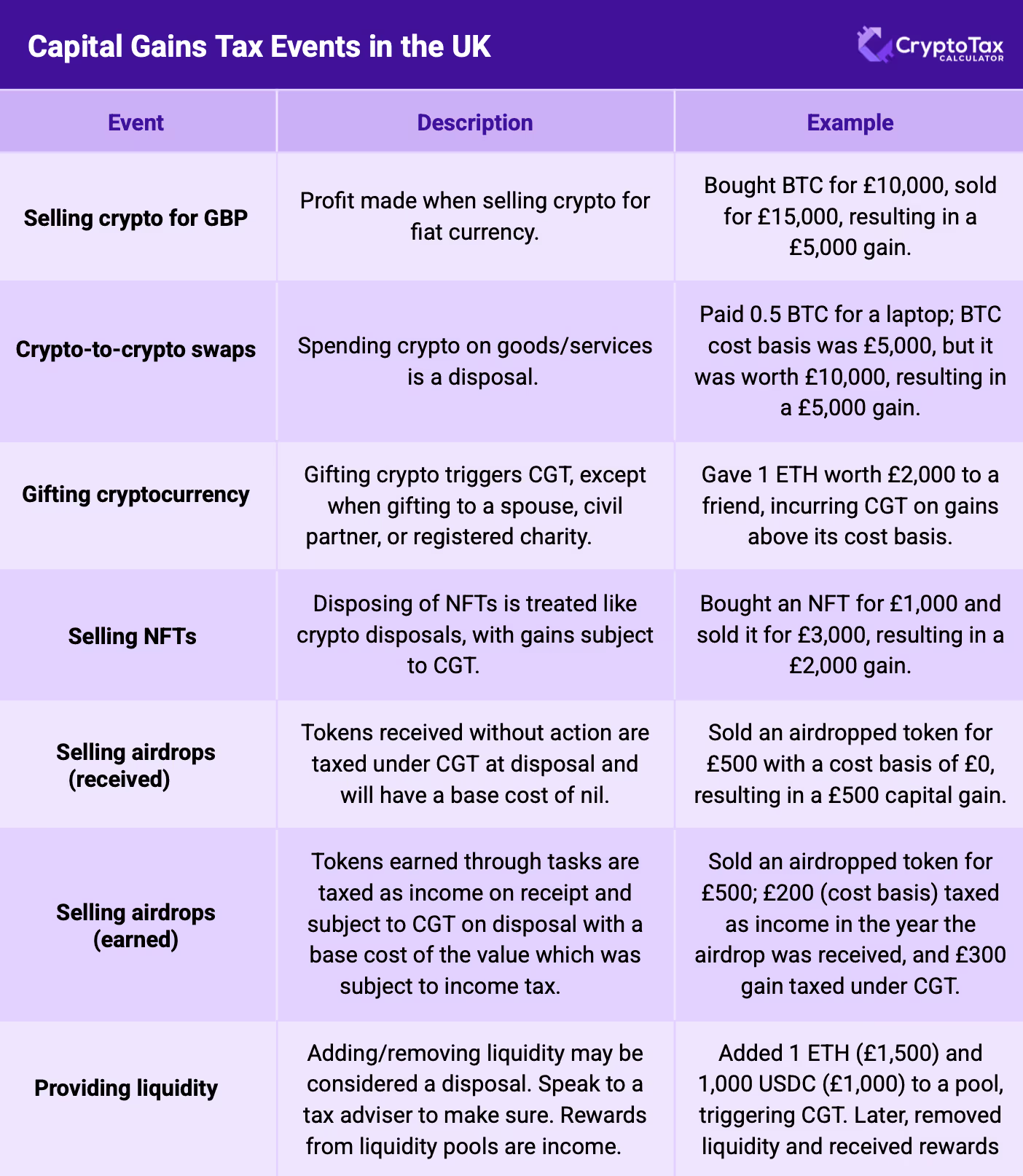

Providing liquidity

Adding liquidity: If adding assets to a liquidity pool results in a change of ownership or creates a new token (e.g., LP tokens), it may be considered a taxable disposal, with CGT applying to any gains. The answer to this can usually be found within the terms and conditions of the protocol.

Removing liquidity: Removing assets from a liquidity pool may also be a disposal, potentially triggering CGT based on the gain or loss relative to the cost basis.

Liquidity pool rewards are generally treated as taxable income upon receipt, subject to Income Tax.

Selling airdropped tokens

Selling tokens received through an airdrop is a taxable disposal.

Tokens received without any action (eg, unsolicited distributions) are not taxed as income upon receipt. Instead, they are subject to Capital Gains Tax (CGT) when sold, with the cost basis typically being zero or the fair market value at the time of receipt if explicitly stated by HMRC.

Tokens earned through performing tasks (eg, completing activities) are taxed as income at the market value in GBP upon receipt. When sold, the gain or loss is subject to CGT, calculated using the market value at receipt as the cost basis.

Example: You perform a series of tasks to qualify for an airdrop. You then sell that airdropped token for £500 and it has a cost basis of £200. The £200 cost basis would have been subject to income tax in the tax year in which it was received and the £300 gain is subject to CGT in the tax year in which the token is sold.

Selling NFTs

Disposing of NFTs is treated similarly to crypto disposals, with gains subject to CGT.

Example: If you bought an NFT for £1,000 and sold it for £3,000, the £2,000 profit is taxable.

Gifting cryptocurrency (excluding spouse or civil partner)

Gifting crypto to someone triggers CGT based on the market value at the time of the gift. Gifting to registered charities or your spouse or civil partner does not trigger a taxable event. Here, we have often seen individuals gifting tokens to others but keeping them in their own wallet. If this is the case, it is very important to document the gift. Consider speaking to a tax advisor if you are uncertain of your position.

Example: Giving 1 ETH to a friend worth £2,000 incurs CGT on any gains above its cost basis.

Using crypto to purchase goods or services

Spending cryptocurrency on goods or services is considered a disposal.

Example: Paying 0.5 BTC for a laptop is a taxable event. If the BTC had a cost basis of £5,000 but was worth £10,000 at the time of the transaction, the £5,000 gain is subject to CGT.

Crypto-to-crypto trades (swaps)

Exchanging one cryptocurrency for another (e.g., BTC for ETH) is treated as a disposal for tax purposes.

Example: Swapping BTC worth £5,000 for ETH creates a taxable event, with any profit based on the cost basis of your Bitcoin. The value of the BTC when swapping will be the proceeds and will also become the cost of the ETH that has been obtained.

Selling crypto for GBP

Any profit made when you sell crypto for fiat currency (e.g., GBP) is a taxable event.

Example: If you bought BTC for £10,000 and sold it for £15,000, you have a taxable gain of £5,000.

How Investing vs Trading impacts tax

In most cases of buying and selling cryptocurrency as a retail investor, you are participating in investing rather than trading. The two are treated differently for tax purposes.

Investing is subject to capital gains tax or income tax, depending on the nature of the transaction.

Trading in this case refers to self-employment which is subject to income tax and National Insurance Contributions.

The key difference between investing and trading – along with the different tax treatments, is how losses generated in the crypto-activity can be used.

In their guidance, HMRC have explicitly stated that they would expect it to be exceedingly rare that any crypto-activity constituting buying & selling crypto would be classified as “trading”.

If you are uncertain, speak to a tax advisor as there are always exceptions, including but not limited to, developing tokens and large scale mining.

How is crypto tax calculated in the United States?

You can be liable for both capital gains and income tax depending on the type of cryptocurrency transaction, and your individual circumstances. For example, you might need to pay capital gains on profits from buying and selling cryptocurrency, or pay income tax on interest earned when holding crypto.

Download your crypto transaction history from all exchanges and wallets you have used.

Categorise transactions that are subject to Capital Gains Tax or Income Tax and apply relevant HMRC rules.

Deduct eligible fees and offset losses to reduce taxable gains and save on taxes.

Use software like Crypto Tax Calculator to automate the process for you, help reduce errors, and make tax time stress free.

This tax guide is regularly updated: Last Update

In the UK, His Majesty's Revenue and Customs (HMRC) treats crypto transactions as taxable events, meaning you may owe taxes on your capital gains or income derived from crypto.

This includes crypto-to-crypto transactions, the use of stablecoins, DeFi protocols, and income derived from on-chain activities like yield farming and staking. So if you have been carrying out these types of transactions but not converted your crypto back into fiat currency, you may still be liable for taxes.

This is because the HMRC treats cryptocurrencies as property, rather than currency.

This article provides a detailed step-by-step guide of how to calculate your cryptocurrency taxes in the UK and report them to the HMRC at for each financial year starting on 6 April and ending on the following 5 April.

From identifying taxable events to calculating your liabilities for both Capital Gains Tax and Income Tax, we’ll break down everything you need to know to stay on top of your obligations.

{{crypto-tax-uk-hmrc-callout-2}}

{{crypto-tax-uk-hmrc-callout1}}

{{save-time-with-cryptotaxcalculator}}

Step 1. Record keeping

Before you begin calculating your crypto taxes, you need to ensure that you have accurate records of all your transactions in Pounds Sterling (GBP). These can be obtained from centralised exchanges, usually as a CSV spreadsheet.

If you have been trading on international exchanges, you need to value these transactions in GBP consistently, such as by cross-referencing prices with a local exchange.

If you have been trading on decentralised exchanges (DEXs), then you should consider using specialised tax software (such as Crypto Tax Calculator) to accurately calculate your transaction data. You may also choose to keep manual records, but be aware that this makes it much harder to ensure accurate records, especially if handling complex DeFi transactions.

In addition to tracking your transactions and assets in GBP, you need to keep a record of the following with each transaction:

Date and time of the transaction

Transaction types (e.g., buys, sells, swaps)

Associated fees (e.g., transaction fees, gas fees, margin fees)

Amounts and types of cryptocurrency involved

GBP value of crypto at the time of each transaction

You may also want to record the following information regularly, to make your books easier to review in case of an enquiry.

Cumulative total of the investment units (ie, crypto) held as a result of the transaction

Any relevant wallet addresses and bank accounts

Maintain your records for at least 5 years after the end of the normal submission window for your tax return (i.e. 31 January following the 6 April financial year end)

If you have a lot of trades spread across multiple exchanges and DeFi protocols, then you should consider using crypto tax software like Crypto Tax Calculator which automatically analyses all relevant transaction data for you, calculates your tax owed, and summarises it in a professional report ready for the HMRC.

Step 2. Identify taxable events

Before calculating your crypto taxes, you need to understand which activities trigger a taxable event under UK law.

You will then need to identify any taxable events in the transaction records you made in Step 1.

HMRC treats cryptocurrencies as akin to property or shares, and many transactions involving crypto are considered disposals, which may result in Capital Gains Tax (CGT) or Income Tax, depending on the nature of the transaction.

As such, you will need to divide your taxable events into either CGT or Income Tax events.

{{how-investing-vs-trading-impacts-tax}}

Events subject to Capital Gains Tax

These events occur when you dispose of your cryptocurrency.

"Disposal" includes selling, trading, or gifting crypto assets (except to a spouse or civil partner).

Each event triggers a CGT liability if the transaction results in a gain.

However, recording losses is equally important, as they can offset gains and reduce your overall tax burden.

{{selling-crypto-for-gbp}}

{{crypto-to-crypto-trades}}

{{using-crypto-to-purchase-goods-or-services}}

{{gifting-cryptocurrency}}

{{selling-nfts}}

{{selling-airdropped-tokens}}

{{providing-liquidity}}

{{crypto-tax-uk-hmrc-callout-4}}

Events subject to Income Tax

Certain events are classified as income and are subject to Income Tax instead of CGT. These typically involve receiving cryptocurrency as payment or rewards.

{{staking-rewards}}

{{mining-rewards}}

{{receiving-airdrops}}

{{payments-for-goods-or-services}}

{{yield-farming}}

{{classify-taxable-events}}

Step 3. Apply Special HMRC rules

There are special rules that apply to investment assets like cryptocurrencies. These rules may change how much capital gains tax you owe.

You need to apply these rules before calculating your cost basis and subsequent capital gains tax.

HMRC Special Tax Rules

Same Day Rule

Any trades that you make on the same day with the same cryptocurrency are first grouped together before adding the leftover to the average cost basis pool.

Time

Trade

Price

Quantity

Total Balance

Adjusted Cost Basis

Gain (Loss)

(1)

Jan 2nd 9am

Buy

500

1

1

500

-

(2)

Jan 4th 9am

Buy

1000

1

2

-

-

(3)

Jan 4th 10am

Buy

3000

1

3

-

-

(4)

Jan 4th 11am

Sell

5000

1

2

1,250

3,000

In this scenario the buy transactions on Jan 4th are grouped with an average cost basis of £2,000 and the sell on the 4th is applied to this daily average cost basis, realising a gain of £3,000.

The remaining 1 BTC with an average cost basis of £2,000 is then added to the pool making a new average pool of £1,250.

The same is also true for fees, meaning any fees paid within the same day will also be grouped together.

Time

Trade

Price

Quantity

Fee %

Fee

(1)

Jan 5th 9am

Sell

2000

1

10%

200

(2)

Jan 5th 10am

Sell

2000

1

20%

400

In this scenario, the two sell transactions both occur on the 5th of January, and each have a different fee rate.

Due to the Same Day rule, the fees for these two transactions are grouped, resulting in an average fee rate of 15%.

Within Crypto Tax Calculator, the value of the fee shown in the transaction breakdown table will be based on this calculated average fee for all transactions within the same day, rather than the rate for the individual transaction.

That is, each transaction will show a 15% fee rate, with the value of the fee being £300 for each, rather than £200 for the first transaction and £400 for the second.

Bed and Breakfast Rule

To avoid people taking advantage of the average cost basis, and tax free threshold, the government introduced the bed and breakfast rule, named after a tax loss harvesting strategy where investors would sell their stock on the last day of the financial year and buy it back the next day.

This rule essentially states that if you buy back the cryptocurrency within 30-days of its disposal, regardless of the tax year, you will “void” the capital gains event previously associated with this transaction, and instead rematch the buy and the sell.

Example: Buying back within 30 days

Violation of Bed and Breakfast rule

Date

Trade

Price

Quantity

Gain (Loss)

(1)

1st January

Buy

10,000

1

-

(2)

3rd April

Sell

13,000

1

3,000

(3)

8th April

Buy

14,000

1

-

You buy 1 BTC with an average cost of £10,000.

You then sell the BTC aiming to realise a gain of £3,000 in this tax year to use up the new £3,000 tax-free allowance. You then re-buy the BTC in the next financial year, with the new average cost basis being £14,000 per BTC.

However, the rules per the example below would apply and the gain is effectively “nullified”.

Apply Bed and Breakfast rule

Date

Trade

Price

Quantity

Gain (Loss)

(1)

1st January

Buy

10,000

1

-

(2)

3rd April

Sell

13,000

1

(1,000)

(3)

8th April

Buy

14,000

1

-

The correct application of the BnB rule matches the re-buy with the sells in the last 30 days. In this case we adjust our gain to a loss of £1,000.

Additionally, the average cost basis continues to be £10,000 per BTC.

Step 4. Calculate your Average Cost Basis

If the special cost basis rules do not apply, then you need to use the average cost basis, also known as a section 104 pool, to calculate the cost on capital gains.

For example, if you buy 1 BTC at £1,000 and a second BTC for £3,000, your average cost would be £2,000.

Date

Trade

Price

Quantity

Total Balance

Average Cost Basis

Gain (Loss)

(a)

1st January

Buy

1,000

2

2

1,000

-

(b)

3rd January

Buy

3,000

2

4

2,000

-

(c)

6th February

Sell

4,000

1

3

2,000

2,000

In the above example, you can see how the Average Cost Basis increases from (a) to (b), and a capital gain is realised against this average cost at time (c).

Step 5. Deduct fees

Deduct transaction fees (in GBP) from your gains to reduce your taxable amount.

HMRC's rules specify that only costs that are "wholly and exclusively" incurred as part of acquiring, disposing or enhancing the value of the asset can be deducted from your gains.

Fees must be directly incurred for the purpose of acquiring, disposing of, or enhancing the value of the asset. With that in mind, let's look at which fees are likely to be eligble.

Fees likely to be eligble as deductions

Transaction fees: These are fees charged by exchanges or platforms for executing trades.

Gas fees (transactions): If the gas fee is part of a taxable event (e.g., swapping crypto on a DEX), it can be included in the cost basis or deducted from the proceeds.

Fees likely to be ineligble as deductions

The following fees are highly unlikely to be deductible from your tax as they are not directly connected to acquisition or disposal, unless you can demonstrate they were "wholly and exclusively" incurred as part of acquiring, disposing or enhancing the value of the asset:

Deposit and Withdrawal Fees: Costs incurred when transferring fiat or crypto into or out of an exchange. These fees are typically not deductible for CGT purposes, as they are not directly related to the disposal (ie, sale) of crypto.

Gas fees (transfers): Gas fees for transferring crypto to a wallet for the purpose of storage.

How to deduct fees from capital gains

For Sales or Disposals: Deduct transaction fees from the proceeds to calculate your net gain or loss.

Example: You sell ETH for £5,000, incurring a £100 transaction fee. Your taxable proceeds are £4,900.

For Acquisitions: Add transaction fees to the purchase price to adjust your cost basis.

Example: You buy BTC for £10,000 and pay a £50 fee. Your cost basis becomes £10,050.

Why you should keep track of your fees

Reduces taxable gains: Deducting allowable fees lowers the taxable amount, potentially saving you money on your tax bill.

Ensures compliance: HMRC expects detailed records of all fees related to taxable events.

{{stop-overpaying-callout-box}}

Step 6. Calculate your capital gains or losses

Now that you have determined your average cost-basis and appropriately grouped your transactions – including any special rules – you are ready to calculate the capital gains or losses for each taxable event.

What are capital gains and losses?

Capital losses: A capital loss occurs when the sale or disposal of cryptocurrency results in less than its cost basis. Capital losses can be used to offset capital gains in the period in which they are made or they can be carried forwards to use against future capital gains, reducing your overall capital gains tax liability.

Capital gains: A capital gain occurs when you sell, trade, or dispose of cryptocurrency for more than its cost basis.

How to calculate capital gains and losses

Identify the sale price: Determine the value in GBP of the cryptocurrency when it was sold or disposed of. Use the market price at the time of the transaction.

Subtract the average cost basis: Subtract the calculated cost basis (from Step 4) from the sale price to find the gain or loss.

Account for fees: Deduct any associated transaction fees from the sale price. Ensure these fees meet the"wholly and exclusively" criteria to qualify as deductible. You should have calculated these in Step 5.

Example: Calculating a capital gain

Transaction details

Amount (£)

Sale price

30,000

Cost basis

20,000

Trading fee

500

Capital gain

9,500 (30,000 - 20,000 - 500)

Example: Calculating a capital loss

Transaction details

Amount (£)

Sale price per ETH

900

Cost basis per ETH

1,200

Capital loss per ETH

300 loss (900 - 1,200)

How to use losses to offset gains

Losses can be deducted from gains to reduce your overall taxable amount.

Example: If you have £10,000 in gains and £4,000 in losses, your taxable gain is reduced to £6,000.

If your capital losses exceed your gains in a tax year, the excess losses can be carried forward to offset capital gains in future tax years and reduce your tax. To utilise this benefit, you must first report the losses to HMRC in your Self Assessment tax return.

{{tax-lost-harvesting-callout-box}}

{{get-started-free-with-trustpilot}}

Step 7: Calculate income from cryptocurrency activities

When you earn cryptocurrency through activities like mining, staking, or receiving payments, these earnings are subject to Income Tax. You identified these activities in Step 2.

Calculating the taxable income requires determining the market value of the cryptocurrency at the time it is received.

If you have already calculated the market value of your various crypto income-earning activities (e.g., staking, airdrops, and yield farming), you can now add them together to determine your overall crypto income.

Otherwise, following the steps below to calculate your income from crypto:

Record the transaction date: Note the exact date you received the cryptocurrency.

Determine the market value: Find the value of the cryptocurrency in GBP on the day of receipt using a reliable exchange rate. Where tokens are not widely traded, it may be more difficult to obtain this data so records must be kept to support the value reported on your tax return.

Calculate the taxable income: Multiply the amount of cryptocurrency received by its GBP value.

Include in your total income: Add the calculated amount to your overall taxable income for the year.

Example: Mining income

You mine 0.5 BTC on January 15th. The market value of 1 BTC on that date is £20,000.

Include this £10,000 in your Self Assessment tax return under income.

{{if-you-have-alot-of-income}}

Step 8: Calculate your overall crypto tax liability

Once you've calculated your crypto-related capital gains, losses, and income, the next step is to determine your total tax liability (ie, the actual amount of tax you owe based on your crypto activity).

This involves integrating these figures with your other taxable income and capital gains for the year.

Here's how to do it:

1. Combine crypto capital gains with other capital gains

HMRC requires you to report all capital gains for the tax year, not just those from crypto. This includes gains from things like selling stocks and shares.

Add your crypto capital gains to gains from these other sources.

Deduct your annual CGT allowance from the total.

For 2024-2025 and 2025-26, it will be £3,000.

Only the amount exceeding the allowance is subject to Capital Gains Tax (CGT).

Example:

Source

Capital Gain (£)

Stocks

5,000

Crypto (BTC sale)

10,000

Total Gains

15,000

CGT Allowance

3,000

Taxable Gain

12,000

2. Calculate capital gains tax

Use the following rates for gains above the allowance:

18% for basic rate taxpayers.

24% for higher or additional rate taxpayers.

Your rate depends on your total taxable income, including crypto income and other sources.

Taxpayer Type

Taxable Gain (£)

CGT Rate

CGT (£)

Basic Rate Taxpayer

9,000

10%

900

Higher Rate Taxpayer

9,000

20%

1,800

3. Add crypto income to other taxable income

Combine your crypto income (e.g., staking, mining, payments) with your salary, self-employment income, or other earnings.

Apply the standard Income Tax rates to your total taxable income:

Income Band (£)

Tax Rate (%)

Description

Up to £12,570

0%

Personal Allowance

£12,571 to £50,270

20%

Basic Rate

£50,271 to £125,140

40%

Higher Rate

Above £125,140

45%

Additional Rate

Note: For those earning above £100,000 the Personal Allowance is reduced by £1 for every £2 of earnings over £100,000. This is known as “tapering” and can lead to a very high effective tax rate.

Example:

Income Source

Income (£)

Salary

40,000

Crypto Staking Rewards

10,000

Total Taxable Income

50,000

4. Adjust for allowable losses

Deduct allowable capital losses from your total capital gains to reduce your CGT liability.

If losses exceed gains, carry the excess forward to future tax years to offset gains.

Example:

Component

Amount (£)

Total Gains

15,000

Total Losses

(5,000)

Adjusted Gains

10,000

5. Calculate your total tax liability

Add together:

Capital Gains Tax (from Step 2 of this section).

Income Tax (from Step 3 of this section).

Example:

Tax Component

Amount (£)

Capital Gains Tax

1,800

Income Tax (Crypto Income)

2,000

Total Tax Liability

3,800

6. File your taxes

Report all calculations and figures in your Self Assessment tax return.

Ensure crypto income and gains are listed in the designated sections.

It is generally recommended that the “white space” on the tax return is used to provide further details to HMRC of any assumptions made within the calculations.

{{how-to-calculate-crypto-tax-callout-box}}

{{get-started-free-with-trustpilot}}

How DeFi is Taxed in the UK

Decentralised Finance (DeFi) transactions are taxed in the UK based on their nature and the specific activity conducted.

HMRC has not issued extensive DeFi-specific guidance, but applies general cryptocurrency and financial asset tax principles to these transactions.

Here’s an overview of how common DeFi activities are taxed:

An example of this would be answering a survey and receiving tokens in return or receiving a specific token in exchange for trading on a particular platform, such as receiving UNI for trading on Uniswap.

When you sell the airdrop, the cost basis is the market value at the time of receiving the airdrop reward if you have paid income tax on it. If you have received the airdrop without performing an action in return for it, income tax will not be due but the base cost will be nil.

You should talk to your accountant about your individual circumstances.

Using Crypto Tax Calculator, you can classify transactions as an airdrop if it is not considered income, otherwise you can classify the trade as income.

Staking

The HMRC has stated that staking rewards are taxed as income. Crypto Tax Calculator will separate out staking rewards as income earned.

Once you have earned income from staking, the initial value forms the cost basis for your capital gains or loss. In this way you are not “double taxed”.

For example if you receive £10 of ETH for staking, and later sell the ETH for £100, your income is £10 and your capital gain is £90.

For hobby mining Crypto Tax Calculator will calculate your initial cost basis as the market value when receiving the reward.

This market value is also treated as income by the HMRC. As with airdrops, if the mined token has a market value which is nil, no income tax is due but the base cost when you dispose of the token will be nil.

How hard forks are taxed in the UK

Forking essentially creates a new cryptocurrency that will go into its own holding pool.

The cost basis of the forked cryptocurrency is calculated based on the crypto assets already held by the individual.

How selling NFTs is taxed in the UK

The sale of non-fungible tokens (NFTs) is considered a disposal, similar to selling other cryptoassets.

The market value of the NFT in GBP at the time of sale is used to calculate the gain.

Tax forms you may need for crypto

Cryptocurrency investors in the UK need to include specific forms when filing their tax returns to HMRC.

SA100 (Self Assessment Tax Return): This is the primary form used for reporting income and capital gains. Include a summary of your total crypto gains or losses in the appropriate section.

SA108 (Capital Gains Summary): This supplementary form is for reporting detailed information about disposals of assets, including cryptocurrency. You must list each transaction, including date, sale proceeds, and allowable costs.

Employment Supplementary Pages: If you received crypto as income (e.g., from mining or staking), you’ll need to report it as employment income on the relevant supplementary pages.

The information provided on this website is general in nature and is not tax, accounting or legal advice. It has been prepared without taking into account your objectives, financial situation or needs. Before acting on this information, you should consider the appropriateness of the information having regard to your own objectives, financial situation and needs and seek professional advice. Crypto Tax Calculator disclaims all and any guarantees, undertakings and warranties, expressed or implied, and is not liable for any loss or damage whatsoever (including human or computer error, negligent or otherwise, or incidental or Consequential Loss or damage) arising out of, or in connection with, any use or reliance on the information or advice in this website. The user must accept sole responsibility associated with the use of the material on this site, irrespective of the purpose for which such use or results are applied. The information in this website is no substitute for specialist advice.

FAQ

What is the crypto tax threshold in the UK?

For the 2023-2024 tax year, the CGT allowance is £6,000. It will reduce to £3,000 in 2024-2025.

How do I report crypto gains to HMRC?

Use the SA100 and SA108 forms to declare your crypto gains. Provide detailed information, including sale proceeds and cost basis.

Do I have to pay tax on crypto in the UK?

Yes. Capital gains tax applies to disposals, and income tax applies to crypto received as earnings.

How does HMRC track crypto transactions?

HMRC collects data from crypto exchanges and uses blockchain analytics to monitor transactions.

Is staking crypto taxable in the UK?

Yes. Staking rewards are treated as taxable income at the time of receipt.

What if you forgot to report crypto on your taxes?

Forgetting to report crypto taxes can lead to penalties, depending on the reasons for the error: - Careless errors: Penalty up to 30%. - Deliberate errors: Penalty up to 70%. - Concealment: Penalty up to 100%. If you realise you’ve made an error, you can amend your return within 12 months of the original filing deadline. Consider using the HMRC’s Voluntary Disclosure Program to rectify significant errors.

What happens if I don't pay crypto tax in the UK?

Penalties can range from fines to prosecution for deliberate non-compliance. HMRC have up to 20 years to launch an enquiry if certain conditions are met.

How do I reduce crypto taxes in the UK?

Strategies include utilising tax allowances, tax loss harvesting, and the utilisation of corporate entities (in certain circumstances).

What if you forgot to report crypto on your taxes?

Forgetting to report crypto taxes can lead to penalties, depending on the reasons for the error:

Careless errors: Penalty up to 30%.

Deliberate errors: Penalty up to 70%.

Concealment: Penalty up to 100% (Source).

If you realise you’ve made an error, you can amend your return within 12 months of the original filing deadline (i.e. 31 January). Consider using the HMRC’s Cryptoasset Disclosure facility to rectify significant errors. If you are considering doing this, it is recommended to consult a tax advisor who has experience in making disclosures to HMRC.

James Edwards

Cryptocurrency Expert

James Edwards has been active in the cryptocurrency industry for over 10 years. He is an avid user of DeFi and believes in the promise of a user-owned and operated web.

His expertise as a cryptocurrency journalist has seen him contribute to publications such as Nasdaq, CoinMarketCap and CoinTelegraph.

In the UK, there's a lingering belief among some crypto enthusiasts that their transactions exist in a sort of no-man's land, invisible to the prying eyes of Her Majesty's Revenue and Customs (HMRC). Is this really true?

This guide will walk you through the steps to upload Coinbase data into Crypto Tax Calculator (CTC) by three methods: an API, CSV upload or via OAuth. Uploading your transactions allows CTC to calculate your Coinbase tax obligation.

Learn how Bitcoin is taxed in the U.S., the difference between short and long-term capital gains, and how timing your sale can cut your crypto tax bill.