After you’ve filled out Form 8949 with each crypto transaction, you will need to complete Schedule D by following three steps:

Fill out Part 1 of the form for short-term capital gains and losses

Fill out Part 2 for long-term capital gains and losses

Complete the summary

2025-04-05

Yield farming or DeFi interest

Earnings from yield farming or lending crypto in DeFi platforms are taxed as income at the time they are received. However, depositing into and withdrawing from a liquidity pool may be treated as a disposal, which is a capital gains event.

Example: Earning £500 in interest from a DeFi platform is subject to Income Tax.

Payments for goods or services

Receiving cryptocurrency as payment for goods or services is treated as income at its market value when received. There are instances where the “value” of the work will be taxed instead of the value of the crypto received. Professional advice should be taken if you are unsure.

Example: If you're paid 0.2 BTC for freelance work worth £6,000, this amount is subject to Income Tax.

Receiving airdrops

If you actively participate to receive an airdrop (e.g., completing tasks), the tokens are treated as income at their market value upon receipt.

Example: Earning £100 in tokens from an airdrop after completing tasks is subject to Income Tax.

Mining rewards

Mining rewards are taxed as income. Those undertaking mining activities to an extent to which they are operating a business will be subject to additional tax obligations.

Example: Earning 0.5 BTC through mining worth £10,000 at the time of receipt is subject to Income Tax.

Staking rewards

Cryptocurrency earned through staking is considered income at the market value at the time of receipt.

Example: If you earn 0.1 ETH through staking worth £200, this amount is subject to Income Tax.

Providing liquidity

Adding liquidity: If adding assets to a liquidity pool results in a change of ownership or creates a new token (e.g., LP tokens), it may be considered a taxable disposal, with CGT applying to any gains. The answer to this can usually be found within the terms and conditions of the protocol.

Removing liquidity: Removing assets from a liquidity pool may also be a disposal, potentially triggering CGT based on the gain or loss relative to the cost basis.

Liquidity pool rewards are generally treated as taxable income upon receipt, subject to Income Tax.

Selling airdropped tokens

Selling tokens received through an airdrop is a taxable disposal.

Tokens received without any action (eg, unsolicited distributions) are not taxed as income upon receipt. Instead, they are subject to Capital Gains Tax (CGT) when sold, with the cost basis typically being zero or the fair market value at the time of receipt if explicitly stated by HMRC.

Tokens earned through performing tasks (eg, completing activities) are taxed as income at the market value in GBP upon receipt. When sold, the gain or loss is subject to CGT, calculated using the market value at receipt as the cost basis.

Example: You perform a series of tasks to qualify for an airdrop. You then sell that airdropped token for £500 and it has a cost basis of £200. The £200 cost basis would have been subject to income tax in the tax year in which it was received and the £300 gain is subject to CGT in the tax year in which the token is sold.

Selling NFTs

Disposing of NFTs is treated similarly to crypto disposals, with gains subject to CGT.

Example: If you bought an NFT for £1,000 and sold it for £3,000, the £2,000 profit is taxable.

Gifting cryptocurrency (excluding spouse or civil partner)

Gifting crypto to someone triggers CGT based on the market value at the time of the gift. Gifting to registered charities or your spouse or civil partner does not trigger a taxable event. Here, we have often seen individuals gifting tokens to others but keeping them in their own wallet. If this is the case, it is very important to document the gift. Consider speaking to a tax advisor if you are uncertain of your position.

Example: Giving 1 ETH to a friend worth £2,000 incurs CGT on any gains above its cost basis.

Using crypto to purchase goods or services

Spending cryptocurrency on goods or services is considered a disposal.

Example: Paying 0.5 BTC for a laptop is a taxable event. If the BTC had a cost basis of £5,000 but was worth £10,000 at the time of the transaction, the £5,000 gain is subject to CGT.

Crypto-to-crypto trades (swaps)

Exchanging one cryptocurrency for another (e.g., BTC for ETH) is treated as a disposal for tax purposes.

Example: Swapping BTC worth £5,000 for ETH creates a taxable event, with any profit based on the cost basis of your Bitcoin. The value of the BTC when swapping will be the proceeds and will also become the cost of the ETH that has been obtained.

Selling crypto for GBP

Any profit made when you sell crypto for fiat currency (e.g., GBP) is a taxable event.

Example: If you bought BTC for £10,000 and sold it for £15,000, you have a taxable gain of £5,000.

How Investing vs Trading impacts tax

In most cases of buying and selling cryptocurrency as a retail investor, you are participating in investing rather than trading. The two are treated differently for tax purposes.

Investing is subject to capital gains tax or income tax, depending on the nature of the transaction.

Trading in this case refers to self-employment which is subject to income tax and National Insurance Contributions.

The key difference between investing and trading – along with the different tax treatments, is how losses generated in the crypto-activity can be used.

In their guidance, HMRC have explicitly stated that they would expect it to be exceedingly rare that any crypto-activity constituting buying & selling crypto would be classified as “trading”.

If you are uncertain, speak to a tax advisor as there are always exceptions, including but not limited to, developing tokens and large scale mining.

How is crypto tax calculated in the United States?

You can be liable for both capital gains and income tax depending on the type of cryptocurrency transaction, and your individual circumstances. For example, you might need to pay capital gains on profits from buying and selling cryptocurrency, or pay income tax on interest earned when holding crypto.

Schedule D provides an overall summary of your capital gains and losses.

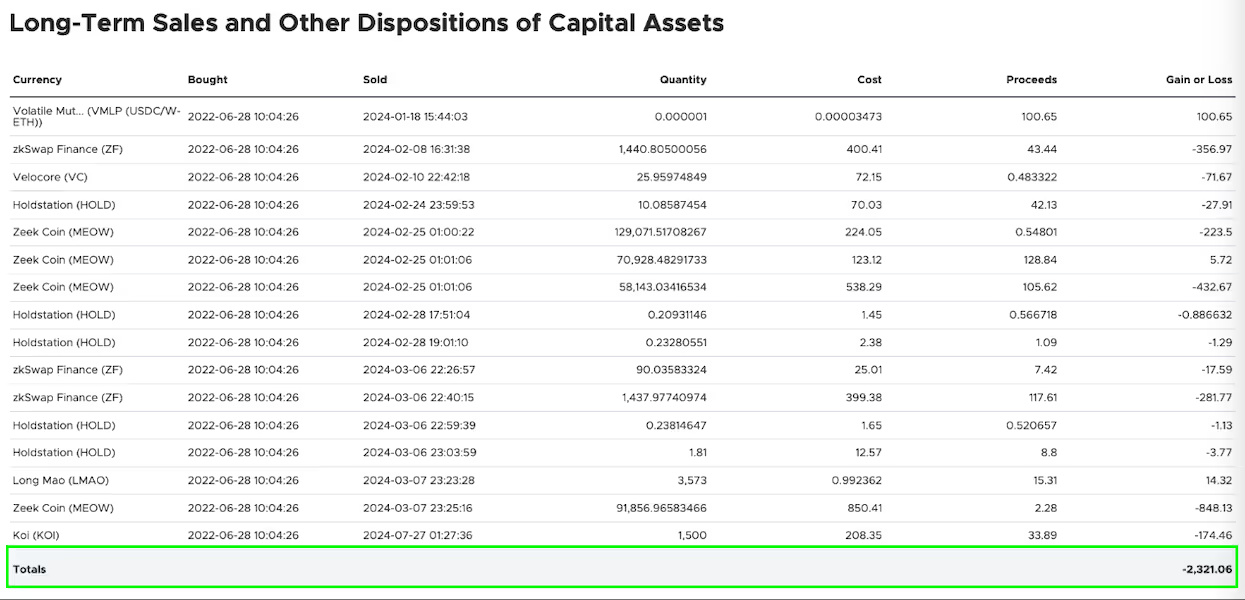

Before completing Schedule D, you have to fill out Form 8949 first, which lists each individual crypto transaction that resulted in a capital gain or loss.

Using Crypto Tax Calculator simplifies the process by automatically organizing your crypto transaction data and creating ready-to-file tax forms for the IRS.

This tax guide is regularly updated: Last Update

It’s the most wonderful time of the year – tax season!

As you get ready to take on your crypto taxes, you might have a few questions. Not sure what Schedule D (Form 1040) is used for? Don’t know the difference between Schedule D and Form 8949? We’ve got you.

In this guide we break down everything you need to know about Schedule D and how to fill it out.

What is Schedule D (Form 1040) Used For?

Schedule D works together with Form 8949, to provide an overview of your capital gains and losses from your investments, including crypto. The total that you report on Form 1040 should be based on your Form 8949 transactions.

Schedule D is broken down into three sections.

Short-term capital gains and losses (if you owned it for less than a year).

Long term capital gains and losses (if you held the asset for over a year).

The sum (total) of the first two sections.

The first 2 sections are further broken down by whether or not the basis was reported to the IRS on a 1099-B.

Most crypto taxpayers do not receive 1099-B’s for their crypto transactions. Therefore, when filling out Schedule D, you want to fill in the appropriate box which indicates whether or not your transactions were reported to the IRS on a 1099-B form.

For short term transactions, this is box C on the 8949 and for Long Term transactions, this is box F on the 8949.

This form is combined with any other income or deductions you may have on Form 1040 so that the IRS can figure out if you owe anything from your investments, or if you should get a refund.

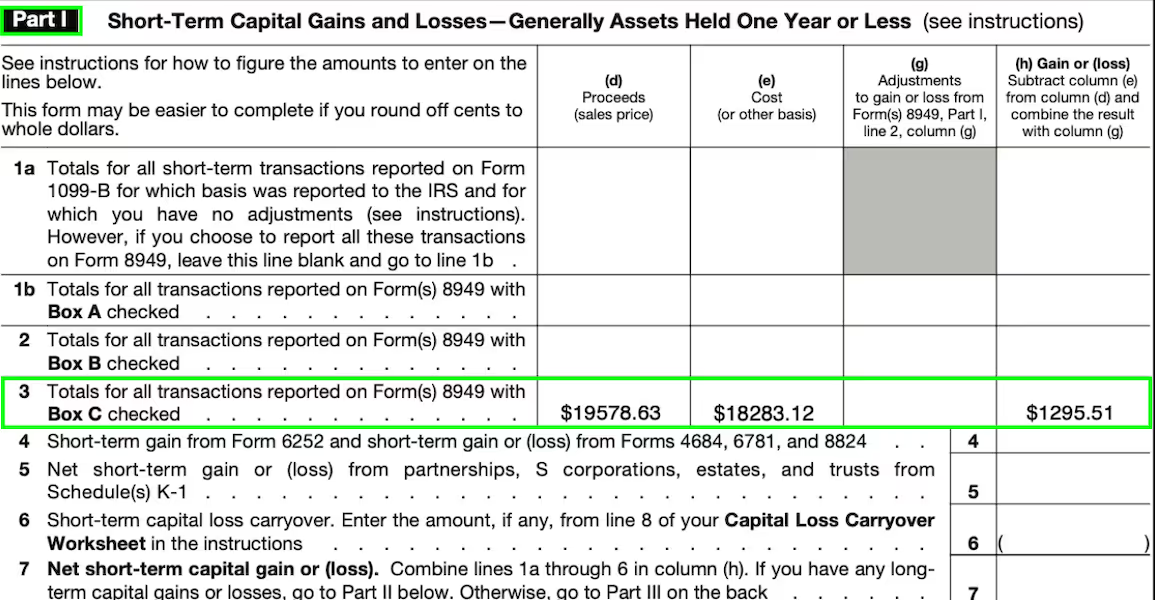

You’ll start by filling out Part 1, which details your short term capital gains and losses from assets that you held for less than a year. To fill this out, refer to the individual gains and losses listed on Form 8949 to calculate the totals for each. You’ll need to state:

Column (d): Total proceeds from the sale

Column (e): The total cost basis

Column (h): The total gain or loss from the transaction

Look out for line 6, where you will report any short-term capital loss crossover. Line 7 is where you report your overall short-term capital gain or loss.

CTC tip: You can cross-check this against the Short Term Gains Total section of the Crypto Tax Calculator Capital Gain Report.

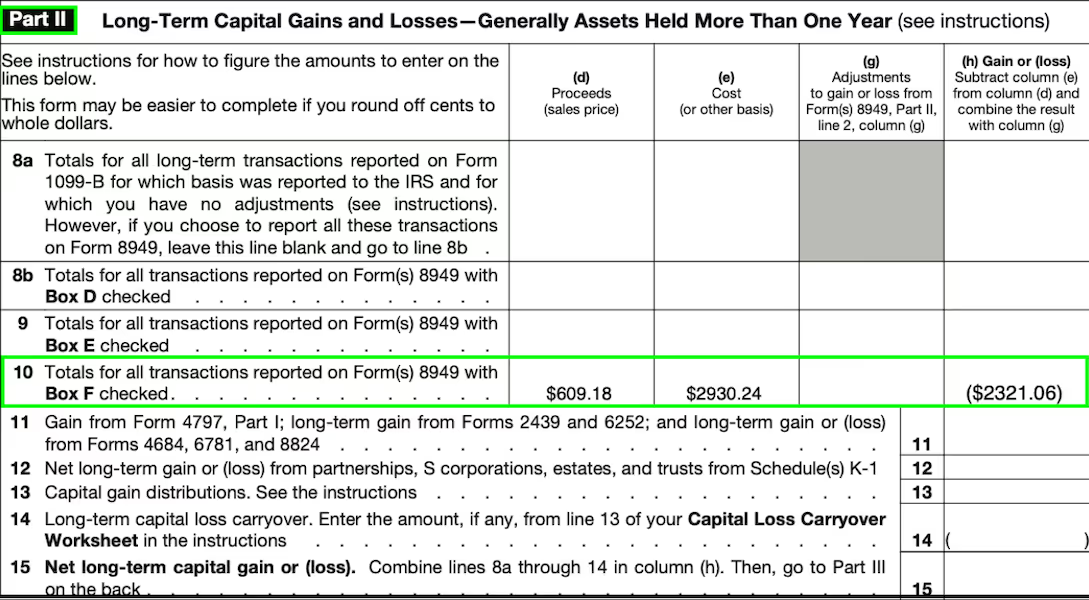

Step 2: Long-term capital gains and losses

Next is Part 2, where you complete your long-term capital gains and losses for assets held over a year. Similar to Part 1, refer to Form 8949 to check the relevant category and then complete:

Column (d): Total proceeds from the sale

Column (e): The total cost basis

Column (h): The total gain or loss from the transaction

Line 14 is where you’ll enter any long-term capital loss carryover, and line 15 is for reporting your overall long-term capital gain or loss.

CTC tip: You can cross-check this against the Long Term Gains Total section of the Crypto Tax Calculator Capital Gain Report.

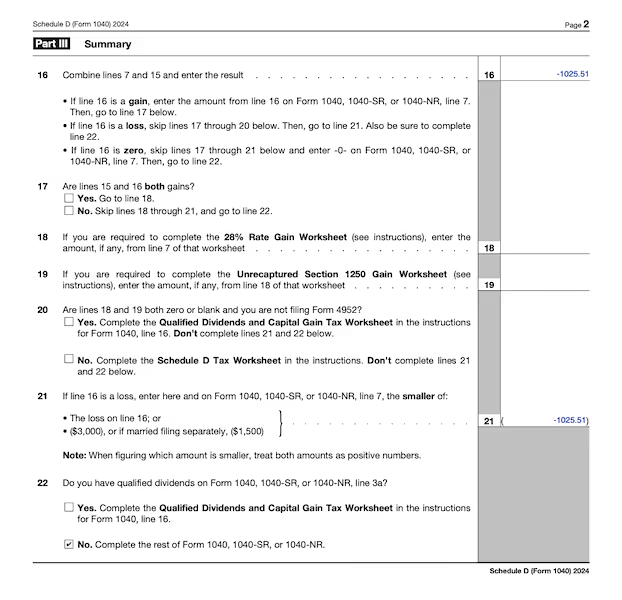

Step 3: Complete the summary

Finally, you complete Part 3 – the summary section that combines Part 1 and 2. On line 16 you write the result of adding line 7 and 15 together to determine your total capital gain or loss.

If there’s a total capital gain, you’ll go to line 17 and complete through 20. However, if there’s a capital loss, you’ll skip lines 17-20 and go to 21 and 22.

Note: You only need to fill out line 21 if you saw a loss on line 16.

CTC tip: If you have a lot of crypto transactions, Crypto Tax Calculator can help out by integrating with all of your crypto platforms to consolidate your transactions on Form 8949 for you. And, it will also generate Schedule D for you, completely filled out.

What Happens After You Fill Out Schedule D?

After you fill out Schedule D, you will have a summary of your capital gains or losses. You will need to report this on Form 1040, line 7 and submit it with the other tax forms outlined below.

How to report your crypto tax with Crypto Tax Calculator

Filling out Schedule D and reporting your crypto taxes is much more simple and time-efficient with Crypto Tax Calculator. Follow these steps to generate accurate reports which meet IRS reporting standards. You can file them with the IRS directly, using software like TurboTax, or hand them over to your accountant.

Get Your Tax Reports Generate comprehensive tax reports ready for your accountant or tax authority.

If you're new to Crypto Tax Calculator, start with our Getting Started Guide for an overview of how the platform works.

Need more help? Visit our US Report Guides or explore the Help Center for step-by-step instructions.

{{how-to-fill-out-schedule-d-form-1040-cta-2}}

Tax forms you need to report crypto

There are several different tax forms you may need to use to report your crypto transactions. While we've already mentioned a majority of them, we'll provide a quick summary so you can ensure you've included all the correct forms when you file your income tax return:

Form 8949: If you sold or otherwise disposed of any crypto in the last tax year, you'll report all information about those transactions on Form 8949, "Sales and Other Dispositions of Capital Assets."

Schedule D (Form 1040): After completing Form 8949, you'll report all of your short-term and long-term capital gains and losses on Schedule D (Form 1040), "Capital Gains and Losses."

Schedule 1 (Form 1040): If you had additional crypto income from staking, mining, airdrops, swaps, or compensation, you'll report it on Schedule 1 (Form 1040), "Additional Income and Adjustments to Income."

Schedule C (Form 1040): If you're self-employed and earned any crypto from clients or other payments, you'll report it on Schedule C (1040), "Profit or Loss From Business."

Form 709: If you gifted any crypto last year and the value exceeds the current gift tax exclusion set by the IRS, you'll have to report the gift on Form 709, "United States Gift (and Generation-Skipping Transfer) Tax Return."

The information provided on this website is general in nature and is not tax, accounting or legal advice. It has been prepared without taking into account your objectives, financial situation or needs. Before acting on this information, you should consider the appropriateness of the information having regard to your own objectives, financial situation and needs and seek professional advice. Crypto Tax Calculator disclaims all and any guarantees, undertakings and warranties, expressed or implied, and is not liable for any loss or damage whatsoever (including human or computer error, negligent or otherwise, or incidental or Consequential Loss or damage) arising out of, or in connection with, any use or reliance on the information or advice in this website. The user must accept sole responsibility associated with the use of the material on this site, irrespective of the purpose for which such use or results are applied. The information in this website is no substitute for specialist advice.

FAQ

Who Needs to File Schedule D (Form 1040)?

Any individual taxpayer who has capital gains or losses resulting from the sale or trade of a property such as crypto will need to report the total on Schedule D.

When Do You Have to File Schedule D?

You have to file Schedule D – along with the rest of your taxes – before the deadline of April 15, unless you have filed for an extension. If you’ve sent Form 4868 off for an extension and it has been approved, then you have until October 15 to file your taxes.

Do I Need to File Schedule D if I Didn’t Receive a Form 1099?

Yes. It doesn’t matter if your crypto exchange didn’t send you a Form 1099, you still need to report your individual capital gains and losses for each transaction on Form 8949 and then the total on Schedule D.

Also, keep in mind that many crypto platforms – particularly DEX’s – do not currently issue Form 1099, so it is up to you to figure out and report your crypto capital gains and losses.

I’m Confused. What’s the Difference Between Form 8949 and Schedule D?

If you’ve experienced capital gains or losses, you will need to fill out both forms. Form 8949 is required to note each individual crypto transaction where you sold or disposed of an individual asset, whereas Schedule D sums up the total capital gains or losses from Form 8949 for your tax return.

On Schedule D you need to report the dates you bought and disposed of the crypto, the cost basis, and the gain or loss.

How Do I Handle Airdrops and Hard Forks on Schedule D?

Airdrops and staking are typically considered taxable income at the fair market value on the date you received the new tokens. They should be reported on Schedule 1 under “Other Income,” not Schedule D. If you decide to sell or trade an airdrop later on, you will need to report any resulting capital gains or losses on Form 8949.

Do I Have To Report Crypto Capital Gains and Losses if They’re Below $600?

Yes. All crypto capital gains and losses must be reported, even if they’re below $600.

While most crypto exchanges only send a Form 1099 when a customer earns at least $600, this is just their threshold for issuing you a form and reporting your transactions to the IRS. It does not mean that you don’t have to report smaller earnings or losses on your tax report.

Nick Waytula

Head of Tax

Nick is a licensed attorney and the Head of Tax at Crypto Tax Calculator, with over 6 years of experience in the crypto tax space. He has previously held key roles at Deloitte and TurboTax, focusing on digital asset taxation and blockchain compliance. At Crypto Tax Calculator, Nick helps drive the development of a leading software that enables taxpayers around the world to accurately and efficiently complete their crypto taxes.

Learn how Bitcoin is taxed in the U.S., the difference between short and long-term capital gains, and how timing your sale can cut your crypto tax bill.

.jpg)