In most cases of buying and selling cryptocurrency as a retail investor, you are participating in investing rather than trading. The two are treated differently for tax purposes.

Investing is subject to capital gains tax or income tax, depending on the nature of the transaction.

Trading in this case refers to self-employment which is subject to income tax and National Insurance Contributions.

The key difference between investing and trading – along with the different tax treatments, is how losses generated in the crypto-activity can be used.

In their guidance, HMRC have explicitly stated that they would expect it to be exceedingly rare that any crypto-activity constituting buying & selling crypto would be classified as “trading”.

If you are uncertain, speak to a tax advisor as there are always exceptions, including but not limited to, developing tokens and large scale mining.

How is crypto tax calculated in the United States?

You can be liable for both capital gains and income tax depending on the type of cryptocurrency transaction, and your individual circumstances. For example, you might need to pay capital gains on profits from buying and selling cryptocurrency, or pay income tax on interest earned when holding crypto.

Reporting your Bitcoin transactions on your federal taxes is essential to comply with IRS regulations.

Whether you've sold Bitcoin for a profit, received it as payment, or earned it through mining, it's important to accurately report these activities.

This guide provides a step-by-step approach to help you navigate the reporting process for the current tax year.

{{how-to-report-bitcoin-on-your-taxes-callout-1}}

{{how-to-report-bitcoin-on-your-taxes-cta-1}}

Step 1: Gather Your Documents

Accurate reporting starts with thorough record keeping.

Collect data summarizing your Bitcoin transactions throughout the year, including sales, purchases, mining, and payments.

Essential information for each transaction includes:

Description of property (i.e., Bitcoin)

Date acquired

Date sold or disposed of

Proceeds

Cost or other basis

Adjustments to your gain or loss

Total gain or loss

Utilizing tax software like Crypto Tax Calculator can streamline this process by analyzing your transaction history once you connect your exchange accounts or wallets.

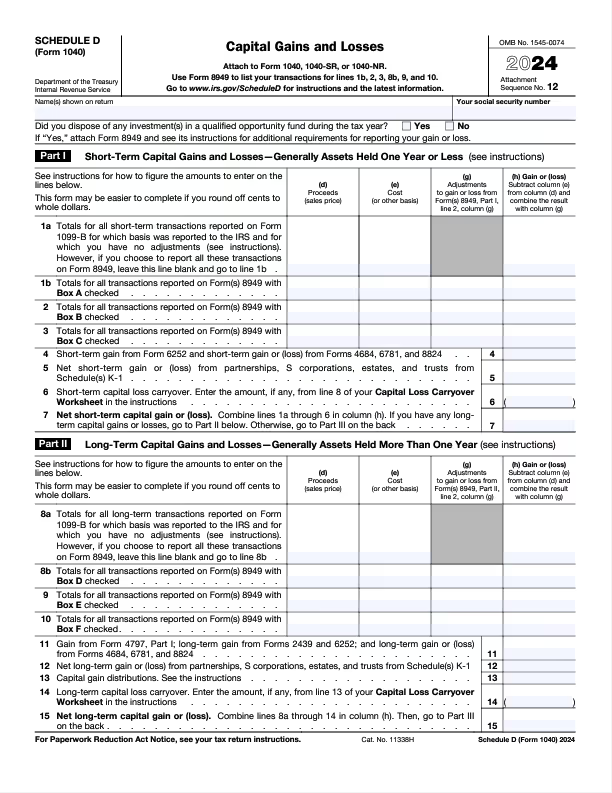

Step 2: Calculate Your Gains and Losses Using Form 8949

Record all Bitcoin transactions on IRS Form 8949, separating short-term (held for one year or less) from long-term (held for more than one year) transactions.

This form helps calculate your total capital gains or losses.

Step 3: Report Your Gains and Losses on Schedule D

Transfer the totals from Form 8949 to Schedule D (Form 1040), which summarizes your overall capital gains and losses.

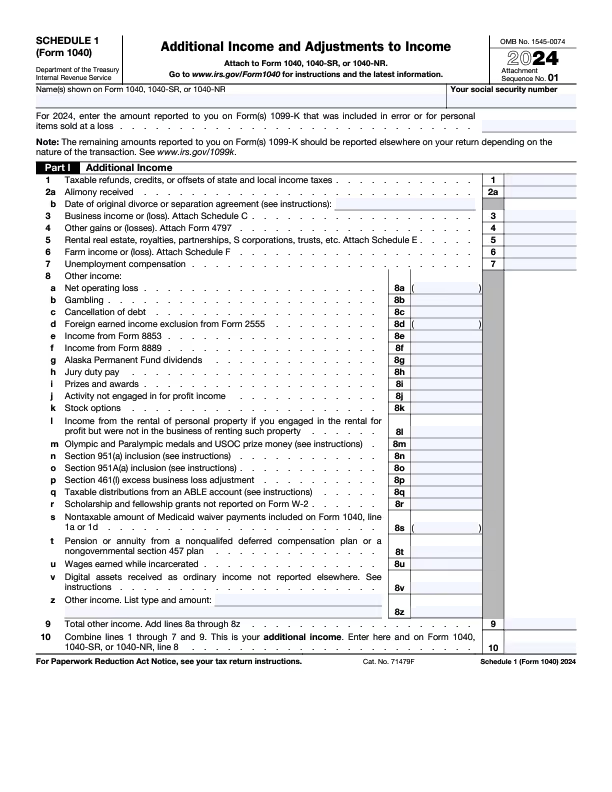

Step 4: Report Any Other Bitcoin Income

If you've earned Bitcoin through mining, staking, airdrops, or as payment for services, report this income on Schedule 1 (Form 1040), Line 8z.

For self-employed individuals receiving Bitcoin as payment, report this on Schedule C (Form 1040).

Step 5: Complete Your Income Tax Return

After accounting for all Bitcoin-related income and transactions, finalize your tax return by including any additional income sources and deductions. Ensure all information is accurate before submitting to the IRS.

{{how-to-report-bitcoin-on-your-taxes-callout-2}}

{{how-to-report-bitcoin-on-your-taxes-cta-2}}

How to Report Bitcoin Losses on Taxes

The IRS allows you to deduct Bitcoin losses to offset gains. For example, if you bought Bitcoin for $5,000 and sold it for $4,500, you can deduct the $500 loss. Report these losses on Form 8949 and Schedule D to ensure they're accurately accounted for.

In years where your losses exceed your gains, you can claim up to a $3,000 net loss to offset other income. Any excess losses can be carried forward to future years.

How to Report Bitcoin Mining Income on Taxes

Bitcoin earned through mining is considered taxable income. Report the fair market value of the mined Bitcoin at the time of receipt on Schedule 1 (Form 1040). If mining constitutes a trade or business, report this income on Schedule C (Form 1040), allowing for the deduction of related expenses.

How to Reduce Your Bitcoin Tax Liability

Consider the following strategies to minimize your Bitcoin tax liability:

Offset Gains with Losses: Sell underperforming assets to realize losses that can offset gains.

Hold Bitcoin for More Than One Year: Qualify for lower long-term capital gains tax rates by holding Bitcoin for over a year.

Invest Through Retirement Accounts: Utilize self-directed IRAs to benefit from tax-free growth on Bitcoin investments.

Donate Bitcoin: Donating appreciated Bitcoin to qualified charities can provide tax deductions and avoid capital gains taxes.

For personalized advice, consult with a tax professional familiar with cryptocurrency taxation.

By diligently following these steps and maintaining accurate records, you can ensure compliance with IRS regulations and effectively manage your Bitcoin tax obligations.

The information provided on this website is general in nature and is not tax, accounting or legal advice. It has been prepared without taking into account your objectives, financial situation or needs. Before acting on this information, you should consider the appropriateness of the information having regard to your own objectives, financial situation and needs and seek professional advice. Crypto Tax Calculator disclaims all and any guarantees, undertakings and warranties, expressed or implied, and is not liable for any loss or damage whatsoever (including human or computer error, negligent or otherwise, or incidental or Consequential Loss or damage) arising out of, or in connection with, any use or reliance on the information or advice in this website. The user must accept sole responsibility associated with the use of the material on this site, irrespective of the purpose for which such use or results are applied. The information in this website is no substitute for specialist advice.

FAQ

No items found.

James Edwards

Cryptocurrency Expert

James Edwards has been active in the cryptocurrency industry for over 10 years. He is an avid user of DeFi and believes in the promise of a user-owned and operated web.

His expertise as a cryptocurrency journalist has seen him contribute to publications such as Nasdaq, CoinMarketCap and CoinTelegraph.

This guide will walk you through the steps to upload Coinbase data into Crypto Tax Calculator (CTC) by three methods: an API, CSV upload or via OAuth. Uploading your transactions allows CTC to calculate your Coinbase tax obligation.

Learn how Bitcoin is taxed in the U.S., the difference between short and long-term capital gains, and how timing your sale can cut your crypto tax bill.

Learn how Bitcoin is taxed in the U.S., the difference between short and long-term capital gains, and how timing your sale can cut your crypto tax bill.