If you’ve earned income or rewards through LP tokens, Crypto Tax Calculator can help you calculate any capital gains or income tax you might owe to the ATO.

Liquidity pools and LP tokens are the backbone of decentralized finance (DeFi), powering many of its innovative financial products.

They make it possible to swap tokens, borrow and lend, farm yields, use aggregators, access on-chain liquidity insurance and more. But while these tools have opened the doors to new financial possibilities, they’ve also introduced new challenges – particularly when it comes to tax reporting and calculations.

In this guide we’ll break down how liquidity pools work, and how to handle the taxes that come with them.

{{ctc-to-manage-defi-taxes}}

What is a liquidity pool?

A liquidity pool is essentially a group of tokens or assets locked into a smart contract to enable decentralized token swaps, lending, borrowing, and other activities, all on-chain.

Each liquidity pool will have a specific composition of assets (usually 2-3 specific tokens) where the amount of Token A + Token B = 'LP AB', and liquidity providers must deposit equal proportions (in market value) of each token to enter the pool.

Liquidity pools form the backbone of decentralized exchanges (DEXes) such as Uniswap, Pancakeswap and Raydium.

Unlike a centralized exchange, DEXes do not use an order book to create the market price.

When you place a buy order on a centralized exchange, you choose the price you want to purchase the asset for, and when that order gets filled, there is a seller on the other side who placed an order and was happy to sell you the asset at the same price, your order gets filled.

Instead, automated market makers (AMMs) govern the liquidity pools in DeFi, and algorithmically balance the pools to determine the price.

Example:

Let's take a theoretical liquidity pool on Uniswap that consists of 100,000 ETH and 10,000 WBTC. This would be a ETH-WBTC Liquidity Pool (LP).

This gives an initial price ratio of 1 ETH : 0.1 WBTC. Let's say that the price of ETH on some major exchanges, such as Binance and Coinbase, starts to fall below this ratio, down to 1 ETH : 0.09WBTC.

There is now an arbitrage opportunity between the centralized exchanges and the Uniswap crypto liquidity pool.

ETH would be purchased from the centralized exchanges and sold to the pool for an immediate profit.

This selling would rebalance the liquidity pool, adding ETH and removing WBTC until an equilibrium is reached between the centralized exchange price and the decentralized liquidity pool price, meaning arbitrage would no longer be profitable.

In practice, this happens constantly and is why the price of assets is generally very similar to the prices on large exchanges.

{{au-liquiditypools-callout}}

The Process of Providing Liquidity

If you’re ready to get involved in this innovative financial system – and take the risk of impermanent loss in exchange for potential returns from trading fees – here’s how the process of providing liquidity typically works:

1. Choose your liquidity pool

Choose a pool based on what tokens you own and are willing to contribute.

Examples of popular liquidity pools are:

- ETH/USDC

- ETH/WBTC

- ETH/DAI

You’ll need to deposit an equal value of each token in the pair to participate.

2. Choose a platform or protocol for your tokens

Not all platforms are created equal – security and testing matter.

- Choose platforms that have been battle-tested and audited for bugs or flaws.

- Examples include Uniswap, Balancer, Curve, and SushiSwap.

- Some liquidity pools offer incentives to entice you to join the liquidity pool, especially if the pool is new. It is important to note that your funds are only as safe as the contract you deposit them into.

Note: Brand new protocols will generally be more risky than larger, well-known, audited ones. However, there is a risk with any DeFi protocol, so think carefully before deciding to join a LP.

3. Provide liquidity via your web3 wallet

Connect your wallet (such as MetaMask) and deposit the required tokens into the pool.

- You must deposit tokens in the right ratio. Example: 1 ETH : 5000 USDC for the ETH/USDC Uniswap liquidity pool.

- The platform will issue LP tokens representing your stake of the pool.

4. Redeem your LP tokens

When you’re ready to exit the pool:

- Exchange the LP tokens back to the liquidity pool for your share of the pooled assets.

- You’ll receive:

- Your original stake (unless impermanent loss occurred)

- Plus your share of trading fees generated over that time period.

If the pool’s token price has shifted significantly during your time as a liquidity provider, impermanent loss may impact the proportion of tokens you receive when you withdraw. However, if no impermanent loss has occurred, you will walk away with the same amount of s you deposited.

{{au-liquiditypools-callout-2}}

Impermanent Loss

Impermanent loss (IL) is a risk that liquidity providers face when contributing to liquidity pools, due to the constant rebalancing. It occurs when the price of one asset in the pool increases or decreases relative to the other.

For example, if WBTC appreciates against ETH in a WBTC/ETH pool, arbitrage traders will remove the now-more-valuable WBTC and add ETH to the pool. As a result, liquidity providers of this pool lose some exposure to WBTC and end up holding more ETH, missing out on the gains they would’ve made by holding WBTC.

The loss is considered 'impermanent' because it may reverse if the token prices return to the same ratio as when the liquidity provider first entered the liquidity pool. However, if the prices don’t return to that ratio before the provider withdraws their funds, the loss becomes permanent.

To offset the risk of IL, traders who use the liquidity pool must pay a trade fee, which gets allocated to the liquidity providers. The more trades that get made, the more fees are earned – potential making up for any loss liquidity providers may experience.

{{au-liquiditypools-3}}

How are liquidity pools taxed?

The process of providing liquidity, and the resultant LP tokens and their properties are a grey area in most tax jurisdictions. It is important that you discuss these transactions in-depth with your personal accountant so they can take into consideration your personal situation, and how these transactions may affect your tax obligations.

When you deposit your tokens into the pool, effectively you are 'disposing' of the tokens (relinquishing control of them) and receiving a Liquidity pool (LP) token, with substantially different properties, in return.

When you deposit your tokens into the pool, you are basically 'disposing' of the tokens (relinquishing control of them) and receiving a Liquidity pool (LP) token, with substantially different properties, in return. According to the ATO this causes a CGT event to occur, with the capital proceeds based on the market value of the token you received.

In addition, when you withdraw crypto from a liquidity pool it triggers a CGT event. The amount you’re taxed is based on the market value of the crypto you withdraw. You will need to know how much your crypto is worth to figure out if you’ve made a capital gain or loss when a CGT event occurs.

{{au-liquiditypools-4}}

{{tax-software-built-for-defi}}

Categorizing Liquidity Pools on Crypto Tax Calculator

Based on ATO guidance, Crypto Tax Calculator treats your liquidity pool activity as follows:

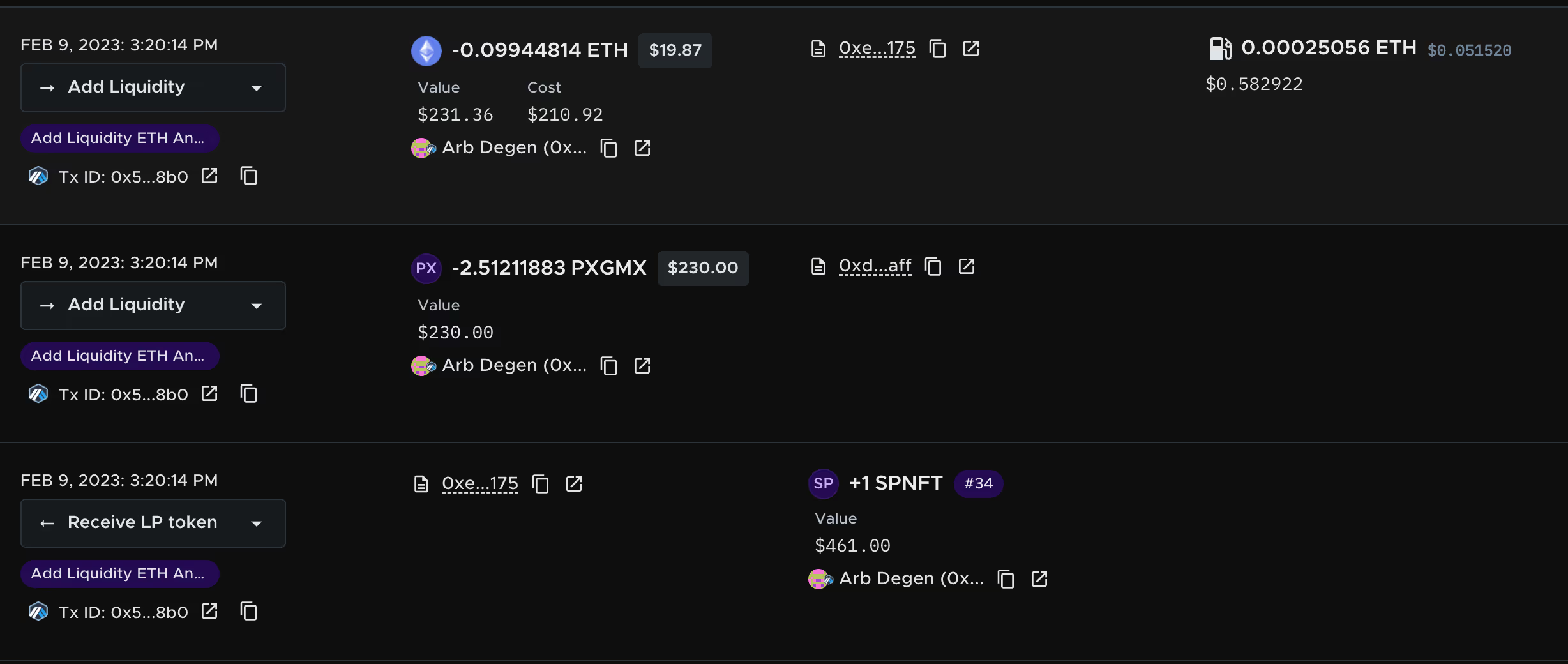

- Depositing into a liquidity pool is categorized as 'Add Liquidity'. This is a capital gains tax (CGT) event, since you’re disposing of the crypto in exchange for LP tokens.

- Receiving the liquidity pool (LP) tokens is categorized as a 'Receive LP Token', with a market value equal to the value of the deposited tokens.

For example, if you deposit pxGMX and ETH digital assets into a liquidity pool on Arbitrum's Camelot DEX, both assets are recorded as 'Add Liquidity' transactions and have an associated capital gain/loss.

The Camelot LP token you receive is recorded as ‘Receive LP Token’ and may have a small associated capital loss due to transaction fees.

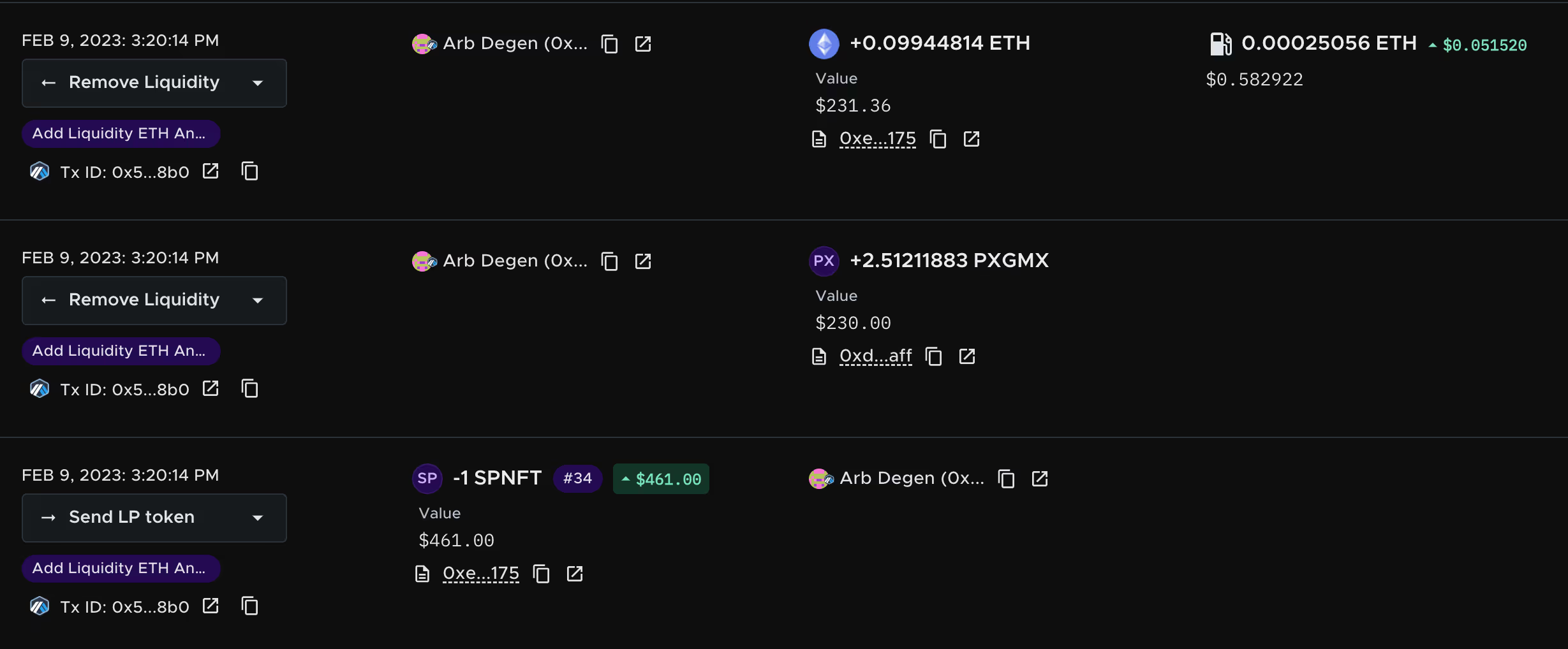

When you withdraw from the pool, the process is reversed:

- Sending your LP token is categorized as a 'Send LP Token'.

- Receiving your original deposited tokens (plus any fees or yield earned) is recorded as 'Remove Liquidity’, which is also a CGT event.

If the LP position has changed in value between the initial deposit and the final withdrawal, this will be classified as a taxable event depending on your tax jurisdiction.

Continuing the example, if you withdraw pxGMX and ETH has been withdrawn from the same Camelot liquidity pool, Crypto Tax Calculator will show:

- A ‘Send LP token’ transaction (with a value match the tokens you’ll receive)

- Followed by separate ‘Remove Liquidity' entries for pxGMX and ETH, each with a capital gain or loss based on the difference in initial value and withdrawal.

Why this matters

Crypto Tax Calculator takes a conservative approach by treating each step of the liquidity pool lifecycle as a taxable event. This ensures our users are well-prepared for any changes in ATO treatment of liquidity pools.

Note: It’s important to confirm your personal tax treatment with a registered accountant, as individual circumstances and interpretations may vary.

{{au-liquiditypools-callout-5}}

LP Token Value

Because there are millions of different liquidity pools – each with their own unique LP token and characteristics – it’s not always possible to assign an accurate market value to your LP token in real time.

The value of an LP token constantly changes as trades occur or liquidity is added or removed. This means the proportion of the pool that your LP token represents is always shifting.

For this reason, Crypto Tax Calculator assigns your LP tokens based on the value of the deposited tokens at the time of deposit. It only receives a new value at the time of withdrawal, based on the market value of the tokens you withdraw.

This method ensures capital gains and losses are properly accounted for, but may result in incorrect 'holdings value' on your dashboard while your LP token is held.

{{au-liquiditypools-6}}

Sources

- Decentralised finance and wrapping crypto, Australian Government: Australian Taxation Office, 2025, https://www.ato.gov.au/individuals-and-families/investments-and-assets/crypto-asset-investments/decentralised-finance-and-wrapping-crypto

The information provided on this website is general in nature and is not tax, accounting or legal advice. It has been prepared without taking into account your objectives, financial situation or needs. Before acting on this information, you should consider the appropriateness of the information having regard to your own objectives, financial situation and needs and seek professional advice. Crypto Tax Calculator disclaims all and any guarantees, undertakings and warranties, expressed or implied, and is not liable for any loss or damage whatsoever (including human or computer error, negligent or otherwise, or incidental or Consequential Loss or damage) arising out of, or in connection with, any use or reliance on the information or advice in this website. The user must accept sole responsibility associated with the use of the material on this site, irrespective of the purpose for which such use or results are applied. The information in this website is no substitute for specialist advice.

FAQ

How do liquidity pools work?

Liquidity pools are an important part of DeFi, enabling users to trade without relying on a traditional order book. Instead of matching buyers with sellers, liquidity pools rely on smart contracts to create a pool of funds that anyone can trade against.

There are different types of liquidity pools – from constant product pools (like Uniswap) to smart pools and algorithmic pools – that each use slightly different formulas to manage trades and maintain price balance.

In general, here’s how liquidity pools work:

- Liquidity providers (LPs) deposit pairs of crypto assets into a pool.

- In return, they receive LP tokens that represent their share of the pool.

- Traders can then swap between the pooled assets, paying a small fee for each trade.

- These fees are distributed equally to LPs, as their reward for providing liquidity.

Liquidity pools vs staking – what’s the difference?

The main difference between liquidity pools and staking comes down to how they work and the level of risk involved.

With staking, you deposit a singular asset in an exchange or wallet to help support the network's operations. In return, you receive rewards – typically in the same token you staked. Staking is typically considered lower risk as you’re not exposed to price fluctuations between multiple assets (as you are in liquidity pools).

Liquidity pools, on the other hand, involve depositing two assets into a pool. These assets are used by traders to swap between tokens, and you receive a share of the trading fees and sometimes additional rewards. However, you’re exposed to a higher level of risk, including impermanent loss. This happens when the relative price of the two assets changes.

Are liquidity pools worth it?

Are liquidity pools profitable? They can be. But, it’s also important to be aware of the fact that you can lose money in liquidity pools. While liquidity providers earn rewards from trading fees, there are several factors that can impact profitability:

- Impermanent loss: This occurs when the value of your deposited tokens in a pool changes in comparison to holding them. If one token in a pair appreciates or depreciates significantly, you may end up with less tokens of the more valuable asset when you withdraw.

- Smart contract vulnerabilities: Liquidity pools run on smart contracts. If the smart contract has a bug or gets hacked, you could be at risk of losing your funds.

- Rug pulls: DeFi rug pulls are becoming more and more common – particularly in newer or unaudited projects. Developers create fake pools or tokens and then disappear with users’ money, leaving behind worthless tokens.

To reduce these risks, stick with reputable platforms, look for audited protocols, and only invest what you can afford to lose.

Patrick has been in the crypto industry for the last 7 years and is passionate about sharing his knowledge and experience in web3. Patrick has also covered the crypto space for Forbes Advisor, Canstar and The Chainsaw.