How to calculate your crypto capital gains tax in 5 steps

1. Identify your crypto transactions 2. Determine the cost basis of your crypto 3. Calculate your proceeds from each sale 4. Calculate your crypto capital gains or losses 5. Report your crypto capital gains or losses via myTax

Using software like Crypto Tax Calculator can help automate this process by importing data from all your wallets and exchanges into one unified tax report. This helps prevent errors and helps you establish an accurate cost basis.

In most cases of buying and selling cryptocurrency as a retail investor, you are participating in investing rather than trading. The two are treated differently for tax purposes.

Investing is subject to capital gains tax or income tax, depending on the nature of the transaction.

Trading in this case refers to self-employment which is subject to income tax and National Insurance Contributions.

The key difference between investing and trading – along with the different tax treatments, is how losses generated in the crypto-activity can be used.

In their guidance, HMRC have explicitly stated that they would expect it to be exceedingly rare that any crypto-activity constituting buying & selling crypto would be classified as “trading”.

If you are uncertain, speak to a tax advisor as there are always exceptions, including but not limited to, developing tokens and large scale mining.

How is crypto tax calculated in the United States?

You can be liable for both capital gains and income tax depending on the type of cryptocurrency transaction, and your individual circumstances. For example, you might need to pay capital gains on profits from buying and selling cryptocurrency, or pay income tax on interest earned when holding crypto.

How to calculate your crypto capital gains tax in Australia

Learn how to calculate crypto capital gains tax in Australia with this step-by-step guide. Understand how cost base works and when you need to figure out capital gains under ATO rules.

Before you can calculate your tax you need to establish a cost base, which includes the original purchase price, fees, and any incidental costs.

Under ATO rules, you have to calculate capital gains or losses anytime you sell, swap, spend, or gift crypto.

The ATO distinguishes between short-term and long-term capital gains, with different tax rates for each.

Crypto tax software like Crypto Tax Calculator makes calculating your capital gains tax faster, easier, and more accurate.

This tax guide is regularly updated: Last Update

Cryptocurrency capital gains refer to the profits you make when you sell, swap, or dispose of your crypto assets for more than you originally paid. Just like with stocks or real estate, these gains are considered taxable events under Australian tax law.

The ATO treats cryptocurrency as a capital gains tax (CGT) asset – like shares or property – not currency. Whenever you dispose of crypto, you may trigger a capital gains tax obligation. Taxable events include selling crypto for AUD, swapping one coin for another, or spending crypto on goods or services.

Understanding how to calculate your gains accurately is essential for staying compliant with ATO regulations and avoiding penalties.

In this guide, we'll explain step-by-step how to calculate your crypto capital gains, how to establish your cost base, and which crypto accounting methods you can use under ATO rules.

Gathering your complete transaction history is the first step in calculating your crypto capital gains. This includes all of your transactions any time you:

Any incidental costs such as brokerage or transfer fees

Example: If you bought 1 ETH for $1,500 and paid a $50 transaction fee, your total cost base would be $1,550.

Cost base becomes more complicated when dealing with multiple purchases of the same asset at different times and prices. In these cases, the accounting method you use (like FIFO or Specific ID) will determine which lot of crypto is sold and what cost base is applied.

The ATO does not endorse a specific method, but many Australian investors use FIFO (first-in, first-out) or Specific Identification methods – as long as they have clear and detailed records.

With that in mind, let’s look at how to use FIFO with specific-wallet accounting to calculate your cost base.

How to establish your cost base using FIFO and Specific Identification accounting

Group transactions by wallet or exchange: You must separate your transactions based on where they occurred. Treat each wallet or exchange like its own inventory.

Match disposals to the appropriate acquisition lot: If using FIFO, your oldest crypto (by acquisition date) is treated as sold first. With Specific ID, you must be able to clearly identify the exact crypto asset sold, including evidence of its purchase date and value.

Track sales in each wallet: Moving crypto between wallets doesn’t trigger a CGT event, but you have to maintain records of the original purchase price and date across your wallets.

Calculate capital proceeds and gains per sale: For each disposal, subtract your cost base from the asset’s market value at the time of disposal to calculate your capital gain or loss.

Note: Once a tax lot is used up (i.e., a specific asset with a cost base is sold) it cannot be used again, and the next oldest asset takes its place as the ‘first asset bought’.

Establishing your cost base for airdrops, gifts and staking rewards:

Airdrops or forks: The cost base may be the fair market value in AUD at the time the asset was received.

Gifts: If you receive crypto as a gift, you generally inherit the giver’s original cost base.

Mining or staking: The cost base is typically the fair market value in AUD at the time the reward was received.

3. Calculate your crypto proceeds

Proceeds refer to the amount you received from disposing of your crypto, before deducting any transaction fees. This is usually the fair market value (FMV) in AUD at the time of sale or exchange.

Example: If you sold 1 BTC for $45,000 AUD, your proceeds are $45,000 AUD.

It's important to capture the FMV accurately at the time of each transaction, as this directly affects your capital gain calculation. You can find the FMV using a reputable exchange like Coinbase.

4. Calculate crypto capital gains or losses

Once you know your cost base and proceeds, you can calculate your capital gains or losses using this formula:

Capital Gain/Loss = Proceeds – Cost Base

In Australia, capital gains tax (CGT) applies when you dispose of a crypto asset by selling, swapping, spending, or gifting it.

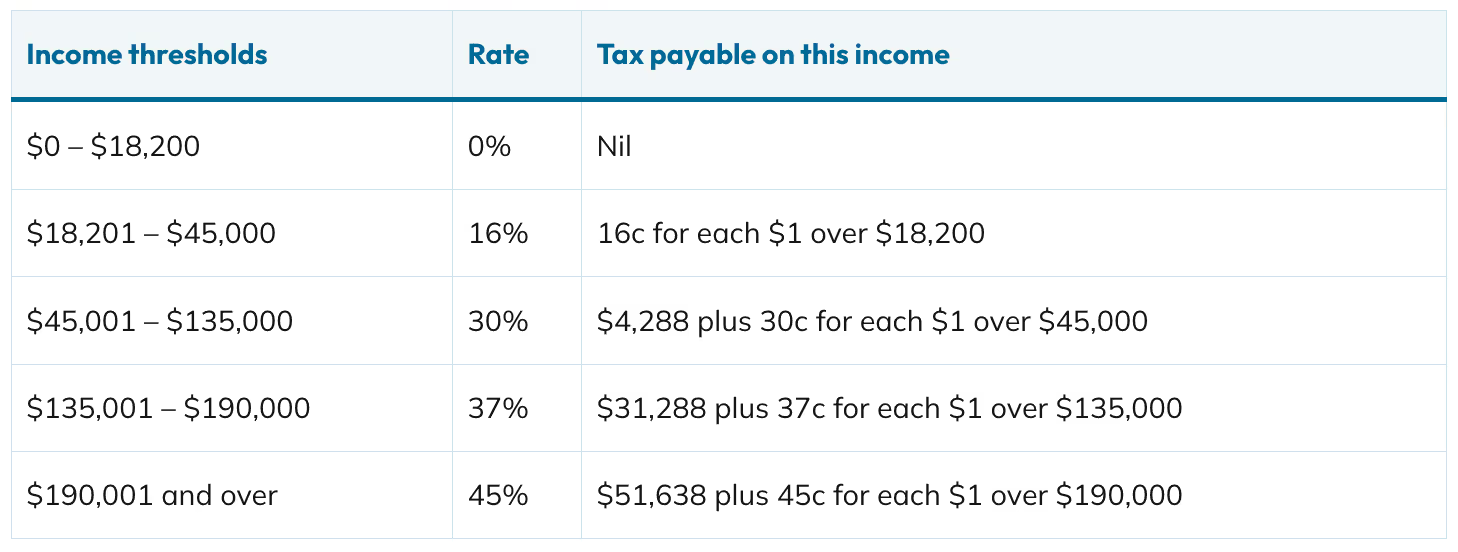

Short-term capital gains tax rates

If you’ve held your cryptocurrency for 1 year or less before selling or exchanging it, your entire capital gain is counted as part of your regular income and is taxed at your ordinary income tax rate. This can range from 0% to 45%, depending on your total taxable income. You may also be subject to the medicare levy of up to 2%.

Holding period was less than 12 months, so this is a short-term capital gain (taxed at ordinary income rates)

Long-term capital gains tax rates

If you’ve held the crypto for more than 1 year, you may qualify for a 50% CGT discount, as long as you’re an individual taxpayer (or investor), not a company (or trader). So, how do you know if you’re an investor or a trader? Here’s an overview:

Investor

Trader

Main purpose

Focused on growing wealth over time by holding crypto

Making quick gains by selling and buying often

How long they hold

Typically over a year

Often short-term – could be days, weeks, or months

How active they are

Trades casually as a hobby or side interest

Trades regularly, maybe even as part of their daily routine

Business setup

Just investing as an individual

Most likely set up as a business, or treats it as one

How they’re taxed

Taxed under CGT rules. They are eligible for the 50% CGT discount if the assets are held for more than a year.

Taxed as regular business income (no CGT discount). They aren’t eligible for the 50% CGT discount.

Note: Just planning to make a profit trading crypto doesn’t make you a professional trader in the eyes of the ATO. They look at your actual activity, business setup, and intent over time to determine where you fit in.

The 50% CGT discount

Holding cryptocurrency for at least one year before selling or exchanging it can significantly reduce your tax liability.

Example (Long-term gain):

Bought 5 ETH at $1,000 each in January 2023

Sold 5 ETH at $2,500 each in February 2025

Capital gain = ($12,500 – $5,000) = $7,500

Holding period was more than 12 months > $3,750 taxable after 50% CGT discount.

Use losses to offset gains

Remember that your losses can be used to offset gains. If your losses exceed your capital gains, the excess can be carried forward to future tax years. In Australia, there’s no annual cap on how much loss you can claim against your income each year.

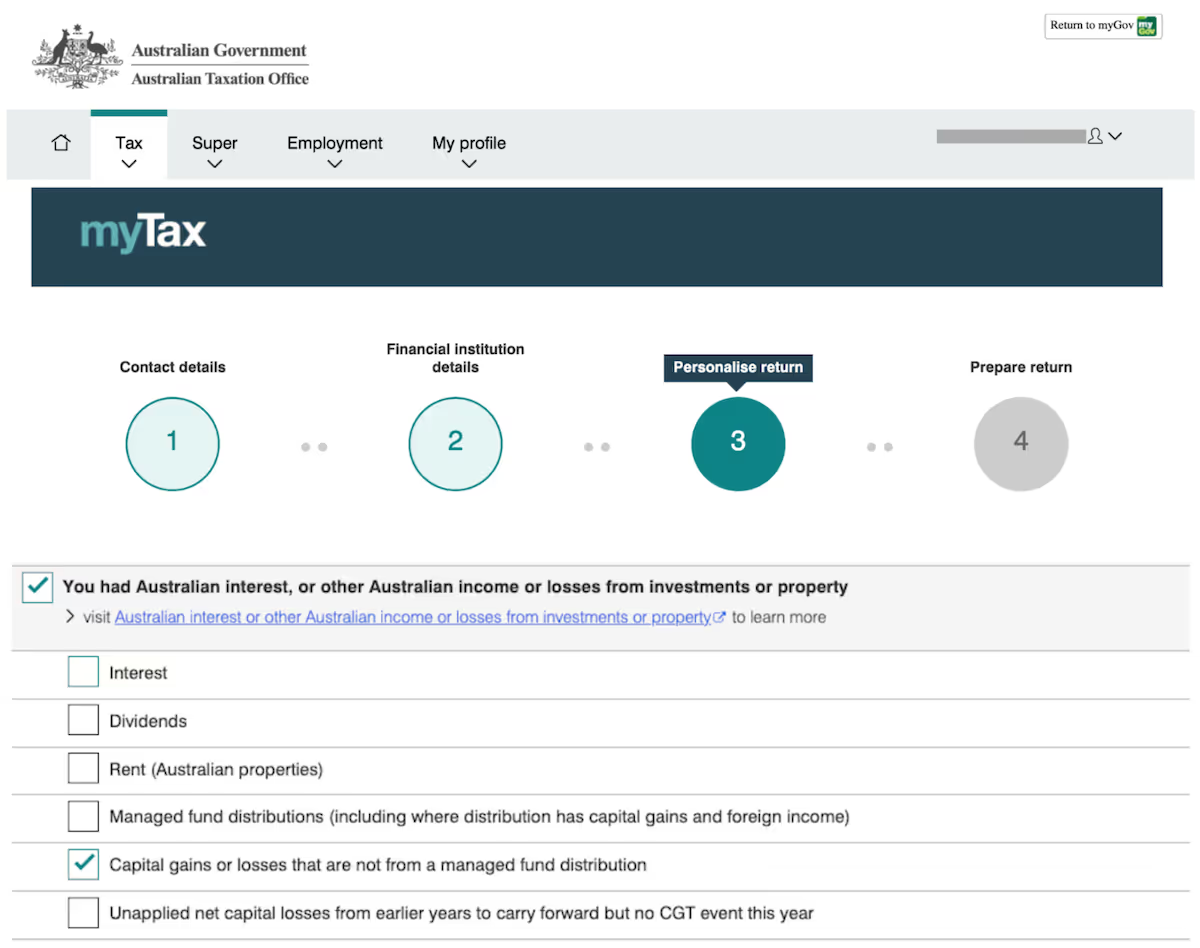

5. Report your crypto capital gains in your Australian tax return

After calculating your gains or losses, you need to report them on your tax return. Specifically:

You’ll need to state each disposal event – such as selling, swapping, or spending crypto – and include details like acquisition date, disposal date, cost base, proceeds, and gain or loss.

Other crypto income: include earnings from staking, airdrops, or yield farming, and report it in the ‘Other Income’ section of your return.

Using Crypto Tax Calculator can simplify this process by importing your crypto transaction data from all your wallets, and generating ATO-ready tax reports you can submit via myTax or send to your accountant.

Accounting Methods: FIFO, LIFO, HIFO, and Specific ID Explained

When calculating crypto capital gains, you need to choose an accounting method to use. This will determine which units of cryptocurrency you’re selling and at what cost base, which impacts the capital gain or loss you report to the ATO.

In Australia, the ATO does not recommend a specific method, but it does ask that your approach is reasonable, well-documented, and consistent. Once you choose a method, you must apply it consistently across all transactions for that tax year.

The most common methods used by investors in Australia are:

FIFO (First In, First Out)

HIFO (Highest In, First Out)

Specific Identification

Note: Methods like LIFO (Last In, First Out) aren’t used commonly in Australia, since they can be harder to justify under the ATO’s expectations of being consistent and reasonable.

FIFO (First In, First Out)

FIFO assumes the oldest crypto you bought is sold first.

Example:

Bought 1 BTC at $10,000 on April 15, 2020 and another at $15,000 on September 2022.

Sold 1 BTC at $20,000 on March 1st, 2025.

Under FIFO, the April 15 BTC is sold first for a capital gain of $10,000.

HIFO (Highest In, First Out)

HIFO prioritizes selling the crypto with the highest cost base to minimise your capital gains and tax liability.

Example:

You own three BTC purchased at $10K, $18K, and $15K, and sell one at $20K. HIFO selects the $18K BTC as the one sold, resulting in a $2K gain.

Specific Identification

Allows you to manually choose the exact units of crypto to sell, provided you have sufficient documentation (including wallet addresses, timestamps, and transaction IDs). This method can be highly tax-efficient when used strategically.

Example:

You hold three ETH purchased at $1,000, $1,500, and $2,000. You sell one ETH at $2,500 and select the $2,000 unit under Specific ID, resulting in a minimised gain of $5,000.

Pros and Cons:

FIFO is simple, commonly used, and easy to justify to the ATO.

HIFO can minimise your short-term gains, but requires detailed records.

Specific ID offers the greatest flexibility and potential tax savings but demands precise tracking and documentation.

HIFO and Specific ID both require flawless record keeping. If the ATO disagrees with your calculations, you may be forced to redo them another calculation.

Crypto Tax Calculator supports multiple methods, helping you compare outcomes and choose the most tax-efficient option.

Capital gains tax events in crypto

Anytime that you dispose of a cryptocurrency, either at a profit or loss, a capital gains event is triggered.

Crypto-to-crypto trades:Swapping one crypto for another is considered a disposal of the original asset, resulting in a taxable event. You must calculate the FMV of the asset received in AUD and use that as the proceeds.

Selling crypto for AUD (fiat): When you sell cryptocurrency for fiat currency (eg, AUD), you must report any capital gain or loss resulting from the sale.

NFTs: Selling NFTs is a CGT event. The gain or loss is based on the difference between your cost base and the sale price in AUD.

Stablecoins: Despite their name, stablecoins experience slight fluctuations in value, and you must report any capital gains or losses, however minor.

Staking rewards and airdrops:Staking rewards and airdrops are treated as ordinary income when received, with that value becoming your cost base for future disposal.

Depositing into liquidity pools: When you interact with DeFi protocols, you often exchange one cryptocurrency for another or for a token representing your stake. This is generally considered a disposal, which the ATO may consider a CGT event.

Considerations when calculating your crypto capital gains tax

Record-keeping: The ATO requires you to keep detailed records of every crypto transaction: dates, values, and purposes. This is essential for accurate reporting and defending your return if audited.

Penalties for incorrect reporting: Failure to report crypto gains accurately can result in penalties, interest, or even ATO audits. The ATO has significantly increased its scrutiny of crypto investors, using data-matching programs with exchanges and wallet providers to track undeclared activity.

Use of crypto tax software: Manual calculation is time-consuming and error-prone. Crypto Tax Calculator can:

Aggregate transactions from 3500+ exchanges, wallets, and DeFi platforms

Automatically apply accounting and inventory methods to help ensure an accurate cost base.

Generate a consolidated crypto tax report in line with ATO requirements

Save you time and help reduce your risk of an audit

The information provided on this website is general in nature and is not tax, accounting or legal advice. It has been prepared without taking into account your objectives, financial situation or needs. Before acting on this information, you should consider the appropriateness of the information having regard to your own objectives, financial situation and needs and seek professional advice. Crypto Tax Calculator disclaims all and any guarantees, undertakings and warranties, expressed or implied, and is not liable for any loss or damage whatsoever (including human or computer error, negligent or otherwise, or incidental or Consequential Loss or damage) arising out of, or in connection with, any use or reliance on the information or advice in this website. The user must accept sole responsibility associated with the use of the material on this site, irrespective of the purpose for which such use or results are applied. The information in this website is no substitute for specialist advice.

FAQ

How do I calculate my cryptocurrency gains?

Subtract your cost basis from your proceeds: Capital Gain = Proceeds - Cost Basis.

What is the cost basis for crypto?

The cost basis is the amount you originally paid for the crypto, including fees.

Do I pay taxes on crypto if I don’t cash out?

Not necessarily. You only owe capital gains tax when you dispose of crypto. However, crypto-to-crypto trades and spending crypto also count as disposals.

Is crypto taxed as short-term or long-term capital gains?

If you hold the asset for less than 12 months, it’s short-term (taxed at ordinary income rates). Over 12 months qualifies as long-term (taxed at lower rates).

How do I report crypto gains on my taxes?

Use Form 8949 for individual transactions and summarize totals on Schedule D. Crypto tax software like Crypto Tax Calculator can help generate these forms. This is especially helpful if you have a large number of transactions to process.

What is the difference between FIFO and LIFO?

FIFO sells your oldest coins first, while LIFO sells your newest. The method affects the cost basis and, therefore, your capital gains.

What is specific ID cost basis?

Specific ID lets you choose which specific units of crypto to sell, allowing for optimized tax outcomes. You must keep detailed records to use this method.

James Edwards

Cryptocurrency Expert

James Edwards has been active in the cryptocurrency industry for over 10 years. He is an avid user of DeFi and believes in the promise of a user-owned and operated web.

His expertise as a cryptocurrency journalist has seen him contribute to publications such as Nasdaq, CoinMarketCap and CoinTelegraph.

Learn how Bitcoin is taxed in the U.S., the difference between short and long-term capital gains, and how timing your sale can cut your crypto tax bill.