Reporting your Bitcoin transactions on your tax return involves a few steps and the following forms:

1. Report capital gains and losses:

Use Form 8949 to list each taxable Bitcoin disposition (sales, trades, spending) with the date, amount, cost basis, and gain/loss.

Totals from Form 8949 flow to Schedule D, where your net capital gain or loss is calculated.

If you have lots of trades, software like Crypto Tax Calculator can generate a consolidated Form 8949 for you.

2. Report Bitcoin income:

Include any Bitcoin you earned as income on the appropriate form. For example, crypto received from mining, staking, airdrops, and other sources would be reported as other income on Schedule 1.

Income from freelance work or other business-related crypto income would be reported on Schedule C. If you were paid via W-2 in BTC, your employer should have converted that to USD on your W-2 already.

3. Answer the IRS Crypto question:

Remember to answer the "Yes/No" question about digital assets on the front of Form 1040. If you had any Bitcoin transactions (other than just buying and holding in your own wallet), you should check "Yes."This includes if you sold, traded, or received Bitcoin in any form.

When using tax filing software, you'll typically find a section to enter cryptocurrency transactions.

Many, such as TurboTax, allow you to upload a file from Crypto Tax Calculator to populate your Form 8949 automatically.

After entering all relevant data, double-check that your totals make sense (e.g. your total Bitcoin sales match any 1099 forms you received from exchanges). Then file as usual. It's a good idea to keep documentation (transaction records, exchange statements) in case of any questions later.

How To Use Crypto Tax Calculator To Calculate Your Bitcoin Taxes

Handling your Bitcoin taxes may seem daunting, but it boils down to applying standard tax principles to your crypto activities.

By keeping thorough records and understanding which transactions are taxable, you can avoid issues and even save money with smart tax planning (like using long-term rates or harvesting losses).

The IRS is paying closer attention to crypto than ever, so compliance is non-negotiable. The good news is you don't have to figure it all out manually.

Bitcoin tax software like Crypto Tax Calculator can automate the heavy lifting. Instead of poring over spreadsheets, you can:

Import all your Bitcoin transactions from exchanges and wallets automatically.

Let the software calculate your capital gains, losses, and income for each transaction.

In short, Crypto Tax Calculator helps ensure you're reporting accurately and not overpaying taxes. It supports integrations with major platforms (from Coinbase to Binance) and handles complex scenarios, so you don't miss a thing.

2025-04-11

How Investing vs Trading impacts tax

In most cases of buying and selling cryptocurrency as a retail investor, you are participating in investing rather than trading. The two are treated differently for tax purposes.

Investing is subject to capital gains tax or income tax, depending on the nature of the transaction.

Trading in this case refers to self-employment which is subject to income tax and National Insurance Contributions.

The key difference between investing and trading – along with the different tax treatments, is how losses generated in the crypto-activity can be used.

In their guidance, HMRC have explicitly stated that they would expect it to be exceedingly rare that any crypto-activity constituting buying & selling crypto would be classified as “trading”.

If you are uncertain, speak to a tax advisor as there are always exceptions, including but not limited to, developing tokens and large scale mining.

How is crypto tax calculated in the United States?

You can be liable for both capital gains and income tax depending on the type of cryptocurrency transaction, and your individual circumstances. For example, you might need to pay capital gains on profits from buying and selling cryptocurrency, or pay income tax on interest earned when holding crypto.

Bitcoin is taxable property, and most transactions are subject to either capital gains or ordinary income taxes.

You must report all taxable Bitcoin events, including sales, trades, and income, to the IRS and pay the necessary taxes (or risk penalties).

Tools like Crypto Tax Calculator simplify crypto tax reporting, allowing you to import your trades and calculate your Bitcoin taxes easily.

This tax guide is regularly updated: Last Update

Bitcoin is the most popular cryptocurrency in the world, making it a great entry point for those who want to dip their toes into crypto investing. However, if you’re hoping to make money from Bitcoin, it’s important to understand the tax implications.

In this in-depth guide, you'll learn how Bitcoin is taxed in the U.S. and how to stay compliant with IRS rules. We’ll cover everything from Bitcoin capital gains tax rules and examples, to reporting Bitcoin on your tax return, and the latest on Bitcoin-specific developments like Ordinals and DeFi.

By the end, you'll understand the key points about taxes on Bitcoin and how to manage your crypto tax obligations confidently.

Continue reading for a complete breakdown of Bitcoin taxes in the U.S., or skip ahead:

In the U.S., Bitcoin and other cryptocurrencies are taxed as property, not as cash. According to IRS guidance, this means that general tax rules for property transactions (like those for stocks or real estate) apply to crypto.

Every time you dispose of Bitcoin (by selling, trading, or spending it), you trigger a taxable event. If you sold Bitcoin (for USD or exchanged it for another coin) for more than you paid, you have a taxable capital gain. If you sold for less than your cost, you have a capital loss (which can offset gains).

Alternatively, some Bitcoin transactions are taxed as ordinary income rather than capital gains. If you received Bitcoin through work, mining, staking rewards, airdrops, or any method, then it's taxed like income, just as if you were paid in USD. The amount of income is the fair market value of the Bitcoin in USD on the day you received it.

Bitcoin Tax Rates: Short-Term vs. Long-Term

When you dispose of Bitcoin that you held as an investment, the profits (or losses) are treated as capital gains (or losses). The tax rate you pay on a Bitcoin gain depends on your holding period:

Short-term capital gains:

If you held the Bitcoin for 1 year or less before selling (starting from the day after you acquire it to the day you dispose of it), it’s a short-term gain.

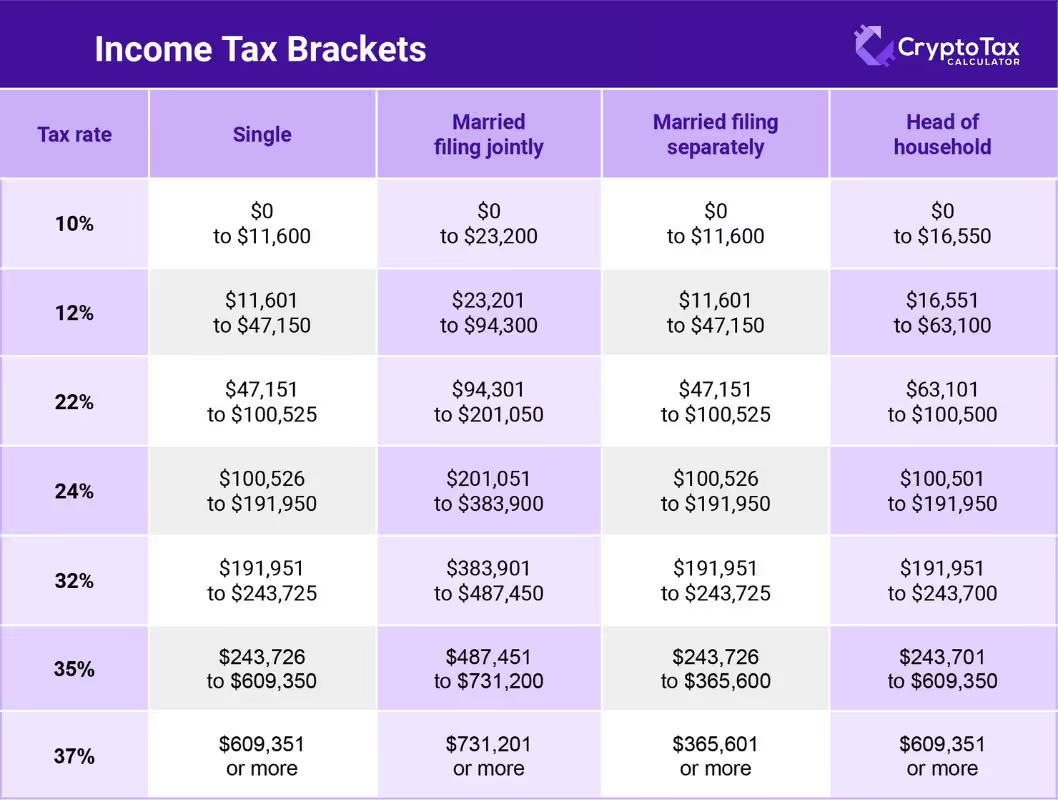

Short-term gains are taxed at your ordinary income tax rates. This rate is based on your income tax bracket for the year (ranging from 10% up to 37% federally).

Long-term capital gains:

If you held the Bitcoin for more than 1 year before selling, it’s a long-term gain. Long-term gains benefit from lower tax rates – 0%, 15%, or 20% at the federal level, depending on your total taxable income.

High-income taxpayers pay 20%, most middle-income folks pay 15%, and some lower-income taxpayers pay 0% on long-term gains.

This distinction is crucial.

Long-term capital gains rates are significantly lower than short-term rates for many people.

For example, a $10,000 Bitcoin profit taken as a short-term gain might be taxed at 22% (if that’s your income bracket), whereas if the same profit were long-term, it might be taxed at 15% or even 0%.

Timing your crypto sales to qualify for long-term treatment can save a lot in taxes — in this case, possibly thousands of dollars.

The tax rate that applies to your Bitcoin transactions depends on a few key factors, including whether you have income or a capital gain, how long you held your Bitcoin before selling, and your taxable income for the year.

Short-term capital gains tax rates

Your Bitcoin income and short-term capital gains (meaning gains on crypto you held one year or less) are taxed exactly the same way.

They’re both taxed at your ordinary income tax rate, just like the income you receive at your job. These tax rates range from 10% to 37%, and the amount you’ll pay depends on your household income.

Long-term capital gains tax rates

Long-term capital gains, meaning gains on assets you’ve held for at least one year, are taxed at either 0%, 15%, or 20%.

The rate you’ll pay depends on your taxable household income. The table below breaks down the three capital gains tax brackets and their corresponding income ranges.

{{bitcoin-tax-callout-3}}

Bitcoin Capital Gains Tax Events

Many people buy and sell Bitcoin on exchanges or trade BTC for other cryptocurrencies. It’s important to know that every trade or exchange is a taxable event under U.S. tax law. Here’s some common taxable events you’ll encounter:

Selling Bitcoin for USD: When you sell BTC for dollars, you have a capital gain or loss based on the difference between your cost basis and the amount you receive when you sell it, minus any fees.

Swapping Bitcoin for other crypto: The IRS considers trading crypto for crypto as two transactions: you “sold” your Bitcoin (triggering a gain/loss) and you bought the new crypto.

Using Bitcoin to buy something: Spending BTC is essentially the same as selling it, at least in the eyes of the IRS. Using crypto for purchases triggers capital gains or losses just like selling it for cash.

Selling Bitcoin for stablecoins: Exchanging Bitcoin for stablecoins is treated exactly the same as disposing of it or swapping it for any other cryptocurrency. You treat it as selling BTC for the dollar value of the stablecoin you received.

Converting wrapped Bitcoin: Even moving BTC to another format can be taxable. For instance, converting BTC to WBTC (Wrapped Bitcoin on Ethereum) could be seen as trading one asset for another (since WBTC is a token distinct from BTC).

Non-taxable events

Moving your own Bitcoin between wallets or exchanges (transfers) is not taxable.

For example, transferring BTC from your Coinbase account to your private wallet isn’t a sale – it’s just a transfer, no different from moving your stock shares from one brokerage account to another without selling them. Just make sure to keep notes so you can later match that withdrawal and deposit as the same coin.

Additionally, buying Bitcoin with fiat is not a taxable event by itself. Tax only comes into play when you dispose of Bitcoin or receive crypto as income.

Bitcoin Income Tax Events

Not all Bitcoin-related tax events are capital gains. Some are taxed as ordinary income.

Here are common scenarios where Bitcoin is taxed as income:

Mining income:Mined Bitcoin is taxable as income upon receipt. When a block reward or mining payout hits your wallet, you should record its USD value at that time. That value is gross income to you.

Staking rewards: Any interest or reward paid in Bitcoin is taxable income at the moment you receive it, measured in USD.

Airdrops: If you receive new coins or tokens for free that are airdropped into your wallet, that’s taxable income.

Bitcoin forks: When a hard fork of Bitcoin occurs, it can result in taxable income. You have to recognize it as ordinary income at the moment you have control over it.

Salary or payments in Bitcoin: If an employer pays you in BTC, or a client pays you in BTC for work, that is wage or self-employment income just as if they paid you in dollars.

All Bitcoin income needs to be reported in USD on your tax return for the year received.

Exchanges or platforms may issue a Form 1099-MISC or other forms if you meet certain thresholds (e.g. Coinbase issues 1099-MISC for staking/interest over $600). But even if you don’t get a form, you are responsible for reporting the income.

New Tax Considerations For Bitcoin Investors

Bitcoin Ordinals and BRC-20 Tokens

Ordinals and BRC-20 tokens are taxed just like other crypto assets or NFTs.

Receiving them for free is considered income, while selling them can result in capital gains and losses. There’s no special tax law just for Bitcoin inscriptions.

You’ll want to keep records of any Ordinal or BRC-20 you deal with (date, value, etc.).

These emerging assets often lack the tax reporting forms that exchanges provide – meaning it’s on you to track them. Using software like Crypto Tax Calculator can help you stay on top of these transactions.

Bitcoin Layer-2 and DeFi

While Bitcoin isn't traditionally associated with DeFi like Ethereum, it still plays a role through layer-2s and other innovations.

The Lightning Network enables fast, low-cost BTC transactions, with tax implications if income is earned.

Sidechains and wrapped BTC (like WBTC) allow smart contract use, but moving BTC into these forms may be taxable.

Earning yield on BTC – through lending or liquidity provision – generates income that's taxed at market value upon receipt.

Using BTC as collateral for loans isn’t taxable, but if the collateral is liquidated, it’s treated as a sale, triggering capital gains or losses.

If in the same year you have some crypto trades with gains and others with losses, the losses will subtract from your gains. For example, if you made a $5,000 profit on one BTC sale but lost $3,000 on another, your net capital gain is $2,000. You’d be taxed only on that $2,000, not the full $5,000 gain.

Excess losses

If your losses exceed your gains, you can use up to $3,000 of the remaining loss to offset other income (like salary) for the year. Any further losses get carried forward to next year.

So, if in 2024 you had no gains and a net $10,000 crypto loss, you can deduct $3,000 of it against your other income (which could save maybe $720 if you’re in the 24% bracket), and carry the remaining $7,000 into 2025. In 2025, that $7,000 can offset 2025’s gains, or another $3,000 can be deducted and the rest carried forward again.

Capital losses carry over indefinitely. If you’re sitting on large unrealized crypto losses from prior years, you can use them in future years when the market rebounds to offset gains (potentially saving a lot of tax). Always track your carryforward losses.

Harvesting losses and the wash sale rule

Tax-loss harvesting is a common investing strategy in which you sell a down asset and use the loss to offset some of your capital gains.

For example, if Bitcoin’s price fell below what you paid, selling to lock in the loss can be beneficial. If you had previously sold Bitcoin for a $2,000 gain but now your holdings are down, you could sell that Bitcoin — or any other asset, for that matter — and reduce your tax burden.

Another thing to consider is that cryptocurrency isn’t subject to the wash sale rule. The wash sale rule, which applies to stocks and other securities, prohibits you from claiming a loss if you buy back the same asset within 30 days before or after the sale. Because crypto isn’t classified as a security, it isn’t subject to the wash-sale rule.

As a result, you can immediately repurchase the BTC you sold while tax-loss harvesting without incurring any penalties.You’ve now got the same amount of BTC, but also a paper loss to help lower your taxes. Just be cautious not to abuse this in ways that might draw IRS scrutiny (always make sure transactions are legitimate market trades).

Keep in mind that the federal government could change its regulations around the wash sale rule later on, choosing to include cryptocurrency. It’s important to consult tax laws and regulations each year to stay up-to-date on any changes.

What about lost or stolen crypto?

Unfortunately, personal losses like lost private keys or crypto stolen in a hack are not deductible as a capital loss. The tax code doesn’t allow a write-off for merely losing access. Casualty/theft losses only apply in very specific events like federally declared disasters since 2018.

Some people with completely worthless coins (from rug-pulls, etc.) have found ways to realize a loss (like selling the token for pennies or abandoning it on an exchange), but simply losing your wallet password doesn’t create a deductible loss.

However, if you had crypto on an exchange that became insolvent (e.g., a 2022 exchange collapse), consult a tax professional – there may be special treatment (e.g., a nonbusiness bad debt or casualty loss claim, though IRS guidance is murky).

{{bitcoin-tax-callout-4}}

{{bitcoin-tax-cta-3}}

We hope this guide has equipped you with the knowledge to navigate Bitcoin taxes in the USA. But remember, whenever in doubt, consult a qualified crypto tax professional. With the rapidly changing landscape, staying informed is key. Good luck, and we've got your back when it comes to simplifying your crypto tax journey!

The information provided on this website is general in nature and is not tax, accounting or legal advice. It has been prepared without taking into account your objectives, financial situation or needs. Before acting on this information, you should consider the appropriateness of the information having regard to your own objectives, financial situation and needs and seek professional advice. Crypto Tax Calculator disclaims all and any guarantees, undertakings and warranties, expressed or implied, and is not liable for any loss or damage whatsoever (including human or computer error, negligent or otherwise, or incidental or Consequential Loss or damage) arising out of, or in connection with, any use or reliance on the information or advice in this website. The user must accept sole responsibility associated with the use of the material on this site, irrespective of the purpose for which such use or results are applied. The information in this website is no substitute for specialist advice.

FAQ

No items found.

Nick Waytula

Head of Tax

Nick is a licensed attorney and the Head of Tax at Crypto Tax Calculator, with over 6 years of experience in the crypto tax space. He has previously held key roles at Deloitte and TurboTax, focusing on digital asset taxation and blockchain compliance. At Crypto Tax Calculator, Nick helps drive the development of a leading software that enables taxpayers around the world to accurately and efficiently complete their crypto taxes.

This guide contains everything you need to know about how to calculate your crypto taxes for the 2024 tax year. It includes crypto tax brackets, crypto capital gains tax, how to report losses, and includes legal ways to lower your bill. Plus how to prepare yourself for some big changes to crypto taxes in 2025.

Learn how Bitcoin is taxed in the U.S., the difference between short and long-term capital gains, and how timing your sale can cut your crypto tax bill.